Golden parachute payments can trigger severe tax penalties that slash the value of your exit package by 20% or more — and most executives don’t realize it until the deal is closing. Under Section 280G of the Internal Revenue Code, if your total change-in-control payments equal or exceed three times your average annual compensation over the past five years, every dollar above your base amount gets hit with a 20% excise tax on top of regular income taxes. Your employer also loses the ability to deduct those excess payments. The good news is that with proper planning and legal guidance, these penalties can often be reduced or avoided entirely through strategic structuring of your change in control provisions.

Key Takeaways

- Section 280G imposes a 20% excise tax (under Section 4999) on “excess parachute payments” — compensation that exceeds your five-year average pay when triggered by a corporate change in control.

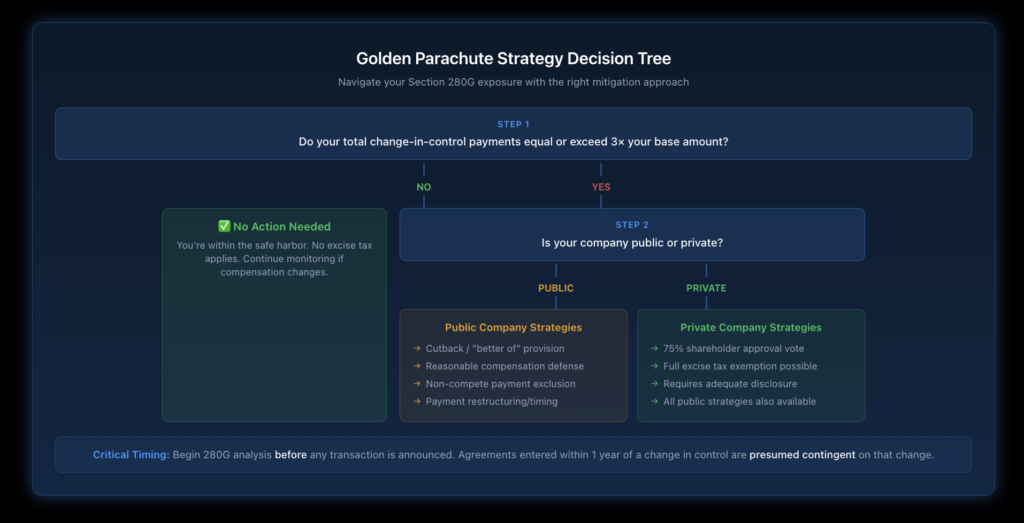

- The three-times-base-amount threshold is a cliff, not a gradual phase-in — crossing it by even $1 subjects the entire excess to penalties.

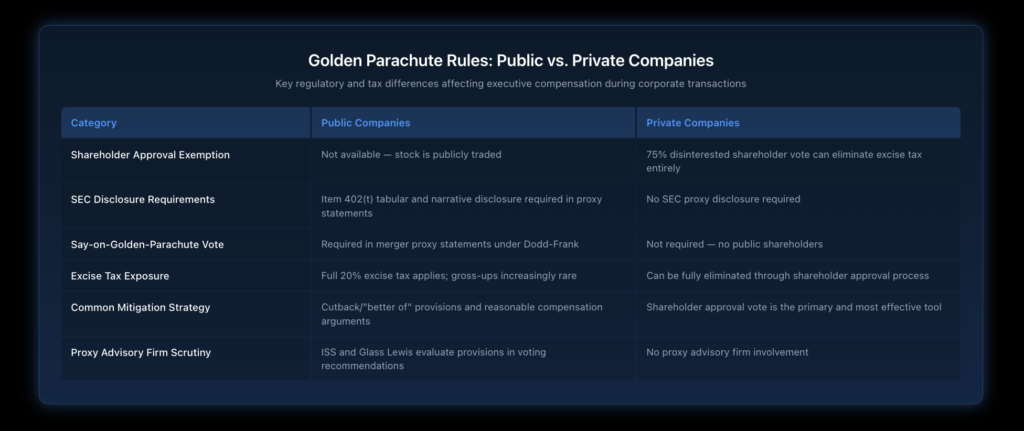

- Private companies can avoid the excise tax entirely through a shareholder approval process requiring 75% of disinterested shareholders.

- Common mitigation strategies include cutback provisions, reasonable compensation arguments, and payment restructuring.

- The Dodd-Frank Act requires public companies to provide say-on-golden-parachute votes during mergers and acquisitions.

- New York executives facing corporate transactions should review their agreements well before any deal closes.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

How Does Section 280G Define a Golden Parachute Payment?

Section 280G was added to the Internal Revenue Code in 1984 to discourage what Congress viewed as excessive executive payouts during corporate takeovers. The law creates a two-part penalty system: the corporation loses its tax deduction for excess parachute payments, and the executive owes an additional 20% excise tax under Section 4999.

What Counts as a “Parachute Payment”?

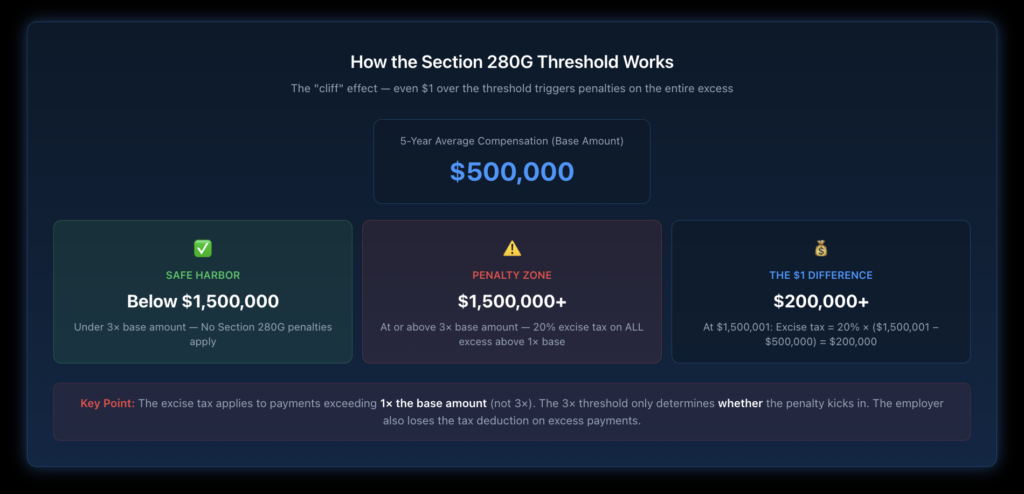

A payment qualifies as a parachute payment when it meets three conditions. First, it must be in the nature of compensation paid to or for the benefit of a “disqualified individual.” Second, it must be contingent on a change in ownership or effective control of a corporation, or a change in ownership of a substantial portion of its assets. Third, the aggregate present value of all such contingent payments must equal or exceed three times the individual’s “base amount.”

The base amount is your average annualized taxable compensation over the five tax years preceding the year of the change in control. Think of it as a rolling five-year average of your W-2 income.

Who Qualifies as a “Disqualified Individual”?

Not every employee is subject to these rules. According to IRS golden parachute regulations, disqualified individuals fall into three categories: shareholders owning more than 1% of the corporation’s stock who provide services, corporate officers, and highly compensated individuals (generally the top 1% of earners, capped at 250 people). If you hold a senior leadership role or have significant equity in the company, you’re almost certainly covered.

How Is the Three-Times-Base-Amount Threshold Calculated?

This is where things get critical — and where many executives get caught off guard. The three-times threshold functions as a cliff, not a sliding scale. If your total parachute payments reach even one dollar at or above three times your base amount, the penalty applies to all payments exceeding one times the base amount.

What Happens When the Threshold Is Exceeded?

Consider this example. An executive has a base amount (five-year average compensation) of $500,000. The three-times threshold is $1,500,000. If total parachute payments come to $1,499,999, Section 280G doesn’t apply at all. But if those payments reach $1,500,001, the excess parachute payment is $1,000,001 ($1,500,001 minus $500,000), and the 20% excise tax would be $200,000.

That’s why even small changes in payment structuring can have enormous financial consequences. It also explains why “cutback” or “haircut” provisions — where payments are voluntarily reduced to just below the threshold — are so common in executive employment agreements.

What Types of Payments Get Aggregated?

Nearly every form of compensation contingent on the change in control gets included in the calculation: severance payments, accelerated vesting of equity compensation, bonus payments, continued benefits, and even non-compete payments. The IRS Golden Parachute Payments Guide makes clear that any payment “in the nature of compensation” counts, including property transfers and stock option acceleration.

Payments made under agreements entered into within one year before the change in control are presumed contingent on that change unless proven otherwise by “clear and convincing evidence.”

What Are the Key Regulatory Frameworks Governing Golden Parachutes?

Golden parachutes sit at the intersection of tax law, securities regulation, and corporate governance. Understanding each layer is essential for executives navigating a potential transaction.

How Does the SEC Regulate Golden Parachute Disclosures?

The Dodd-Frank Wall Street Reform Act created several transparency requirements around executive compensation during corporate transactions. Public companies must now disclose golden parachute compensation arrangements in proxy statements and, in certain circumstances, submit those arrangements to a shareholder advisory vote — commonly called a “say-on-golden-parachute” vote.

Under Item 402(t) of Regulation S-K, both the target and acquiring company must provide tabular and narrative disclosure of all compensation payable to named executive officers that is based on or related to the transaction. This includes severance, accelerated equity, bonus payments, pension enhancements, and tax gross-up payments.

What Role Does the GAO Play in Oversight?

The Government Accountability Office has reviewed the SEC’s implementation of Dodd-Frank golden parachute rules and confirmed that the Commission complied with applicable procedural requirements in promulgating these regulations. This independent oversight helps ensure the regulatory framework is functioning as intended.

What Strategies Can Reduce or Avoid the Section 280G Excise Tax?

This is the most practical question for any executive negotiating performance-based compensation or change-in-control protections. Several legitimate strategies exist to mitigate or eliminate the 280G penalty.

Can a Cutback Provision Protect You?

A cutback (or “haircut”) provision automatically reduces parachute payments to just below the three-times threshold when doing so would leave the executive better off financially. Since the excise tax applies to all payments above one times the base amount, the math often favors keeping payments just under the cliff.

For example, if reducing total payments by $50,000 avoids $200,000 in excise taxes, the cutback makes obvious financial sense. Many executives negotiate a “better of” provision that compares the after-tax result of full payment (with excise tax) against the reduced payment (without excise tax) and applies whichever yields more net cash.

How Does the Shareholder Approval Exemption Work for Private Companies?

Private companies have a powerful tool that public companies don’t: the shareholder approval exemption. If at least 75% of the corporation’s disinterested shareholders approve the parachute payments after receiving adequate disclosure, those payments are completely exempt from Section 280G. This exemption is only available when the corporation’s stock is not publicly traded.

The process requires careful execution. All voting shareholders must receive full disclosure of all material facts regarding the payments. The IRS Revenue Ruling on golden parachute calculations provides guidance on how these determinations are properly made. Missing procedural steps can invalidate the entire exemption.

What Is the Reasonable Compensation Defense?

Even when payments exceed the three-times threshold, Section 280G allows executives to demonstrate that a portion of their payments represents “reasonable compensation” for personal services — either services already rendered before the change in control or services to be rendered after it.

For post-transaction services, this typically involves non-compete agreements. If an executive agrees not to compete with the acquiring company, the non-compete payments can potentially be excluded from the parachute payment calculation. The key requirement is that the non-compete must be enforceable under applicable state law. In New York, where non-compete enforcement is increasingly scrutinized, this defense requires particularly careful structuring.

For pre-transaction services, the executive must prove by “clear and convincing evidence” that they were underpaid relative to comparable executives and that a portion of the parachute payment is actually catching up for below-market compensation.

How Do Clawback Provisions Interact with Golden Parachute Rules?

The relationship between clawback requirements and golden parachute payments creates additional complexity for executives. Under SEC rules, public companies must maintain compensation recoupment policies that can potentially claw back incentive compensation in certain circumstances.

Can Clawback Risk Affect Your Parachute Calculations?

When an executive faces both golden parachute penalties and potential clawback exposure, the financial planning becomes significantly more complex. Payments subject to clawback might ultimately never be received, yet they could still count toward the three-times threshold at the time of the change in control. Working with experienced counsel to coordinate these overlapping provisions is essential.

Executives negotiating departure terms should also consider how deferred compensation and Section 409A compliance requirements interact with golden parachute timing rules. Accelerated payment of deferred compensation triggered by a change in control could push total payments over the 280G threshold even when base salary and severance alone would not.

What Should New York Executives Know About Golden Parachute Planning?

New York adds unique considerations to golden parachute planning. The state’s evolving restrictions on non-compete agreements can directly impact the reasonable compensation defense. If a non-compete isn’t enforceable in New York, the associated payments likely can’t be excluded from the parachute calculation.

How Does New York’s Regulatory Environment Affect Your Options?

New York’s robust wrongful termination protections and strong employee advocacy framework mean that executives have additional leverage when negotiating change-in-control protections. The state’s broader employment protections can sometimes provide alternative grounds for payments that might otherwise be classified as parachute payments.

Additionally, New York executives should be aware of how board compensation committee dynamics influence the structuring of change-in-control packages. Compensation committees at New York-headquartered public companies face particular scrutiny from institutional shareholders and proxy advisory firms regarding golden parachute provisions.

When Should You Start Planning for a Potential Transaction?

The biggest mistake executives make is waiting until a deal is announced to review their golden parachute exposure. Any agreement entered into within one year before a change in control is presumed contingent on that change. That means restructuring payments after a deal is on the table becomes significantly more complicated from a tax perspective.

Ideally, golden parachute planning should happen when you’re first negotiating your executive compensation package — or during regular review periods well before any transaction is contemplated. This gives you the maximum flexibility to structure payments in ways that minimize 280G exposure.

How Does Corporate Governance Influence Golden Parachute Outcomes?

Shareholder activism and proxy advisory firm policies have reshaped how companies approach golden parachute provisions over the past decade. Say-on-pay votes and say-on-golden-parachute votes create real accountability for compensation decisions.

What Trends Are Shaping Golden Parachute Practices?

Several important trends are worth tracking. Excise tax gross-ups — where the company pays the executive’s 280G penalty — have largely disappeared among public companies due to shareholder pressure. Most companies have shifted to cutback or “better of” provisions instead. This means the financial risk of exceeding the 280G threshold increasingly falls on the executive rather than the company.

Additionally, proxy advisory firms like ISS and Glass Lewis evaluate golden parachute provisions when making voting recommendations. Companies with provisions viewed as excessive may face negative say-on-pay recommendations, creating indirect pressure to moderate change-in-control benefits. Executives should understand these dynamics when negotiating their severance and retirement planning arrangements.

Ready to Protect Your Golden Parachute?

If you’re an executive with change-in-control protections — or you’re negotiating a compensation package that includes them — getting ahead of the 280G analysis is critical. The difference between strategic planning and reactive scrambling during a deal can be hundreds of thousands of dollars. Nisar Law Group helps executives across New York and New Jersey understand their golden parachute exposure and develop strategies to protect their compensation. Contact us today for a consultation to review your situation.

Frequently Asked Questions About Golden Parachutes: Tax and Regulatory Issues

The excise tax rate is 20%, imposed under Section 4999 of the Internal Revenue Code. This 20% penalty applies on top of all regular federal and state income taxes the executive already owes on the compensation. The excise tax hits every dollar of “excess parachute payments” — meaning all payments above one times the base amount, not just the amount over the three-times threshold. For a New York executive, the combined effective tax rate on excess parachute payments can exceed 60% when you add federal income tax, state tax, city tax, and the 20% excise tax together.

The base amount is your average annualized includible compensation for the “base period,” which is the five tax years ending before the year the change in control occurs. It’s essentially your rolling five-year average of W-2 compensation (or 1099 income for independent contractors). If you’ve had significant pay increases recently, your base amount may be lower than your current pay, which can make it easier to trip the three-times threshold. This is one reason executives should monitor their base amount calculations annually.

No. The shareholder approval exemption under Section 280G is only available to corporations whose stock is not readily tradable on an established securities market. This means public companies and their executives cannot use this pathway to avoid the excise tax. Public company executives must rely on other strategies, like cutback provisions, reasonable compensation arguments, or careful payment structuring, to manage their 280G exposure.

A “better of” (or “best net”) provision compares two scenarios for the executive and applies whichever produces more after-tax cash. Scenario one is receiving the full golden parachute payment and paying the 20% excise tax. Scenario two is having payments reduced to just below the three-times threshold and paying no excise tax. The provision automatically applies whichever option leaves the executive with more money in their pocket after all taxes are calculated.

Non-compete payments can potentially be excluded from the parachute payment calculation if they qualify as “reasonable compensation for services to be rendered” after the change in control. However, the non-compete must be legally enforceable under applicable state law, and the amount must be reasonable relative to the scope of the restriction. In New York, where courts closely scrutinize non-compete enforceability, relying on this exception requires careful legal analysis and documentation.

When a company gross-ups an executive for the 280G excise tax, it makes an additional payment to cover the tax penalty so the executive receives the full intended compensation. However, the gross-up payment itself is also treated as a parachute payment, which increases the total excess and creates a circular calculation. While gross-ups were once common, shareholder backlash has made them increasingly rare at public companies. Most modern agreements use cutback or “better of” provisions instead.

Ideally, you should assess your 280G exposure when you first negotiate your employment agreement and then revisit it annually, especially if your compensation changes significantly. The one-year presumption rule means that any agreement entered into within 12 months before a change in control is presumed contingent on that change. Waiting until a deal is announced severely limits your options. Proactive planning gives you the most flexibility to structure payments efficiently.