Corporate governance and executive compensation are two sides of the same coin. The board of directors, guided by independence requirements, say-on-pay votes, and federal disclosure rules, decides what your company’s top leaders earn. And if you’re an executive, understanding how those decisions get made—and where shareholders can push back—can mean the difference between a package that protects you and one that leaves you exposed.

Key Takeaways

- Say-on-pay is a non-binding shareholder advisory vote required at least once every three years under the Dodd-Frank Act, giving investors a direct voice in approving executive compensation.

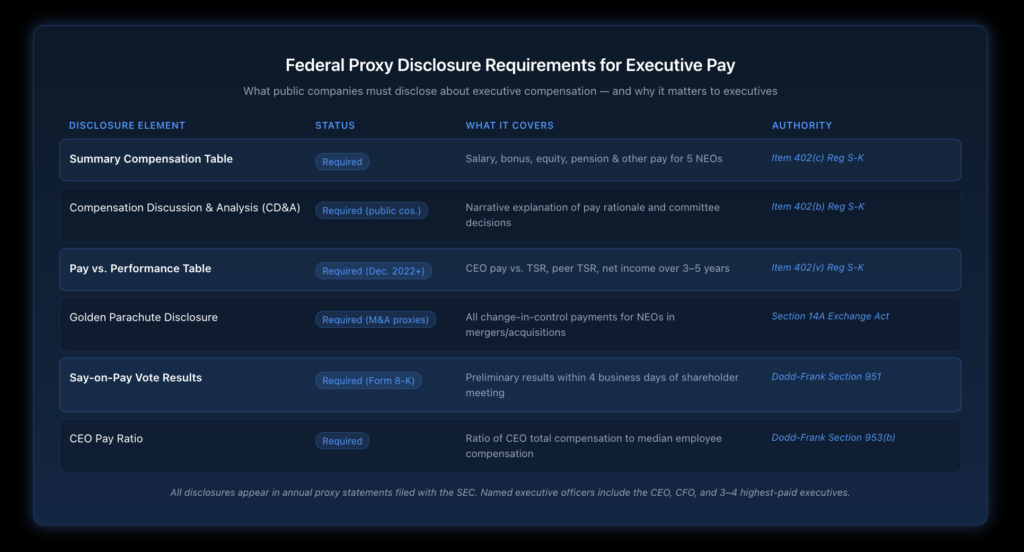

- Proxy disclosures in annual proxy statements must include a Compensation Discussion & Analysis (CD&A) and Summary Compensation Table explaining pay rationale for named executive officers.

- Independent compensation committees are required under NYSE and Nasdaq listing standards, and must evaluate pay through an independence lens.

- Proxy advisory firms like ISS and Glass Lewis wield enormous influence over institutional shareholder votes—and their guidelines treat low say-on-pay support below 70% as a red flag requiring board response.

- Pay vs. performance disclosure, effective for fiscal years ending December 16, 2022, or later, now requires companies to show how CEO pay tracks against financial results.

- New York executives should know that state law adds additional shareholder rights considerations beyond federal minimums.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

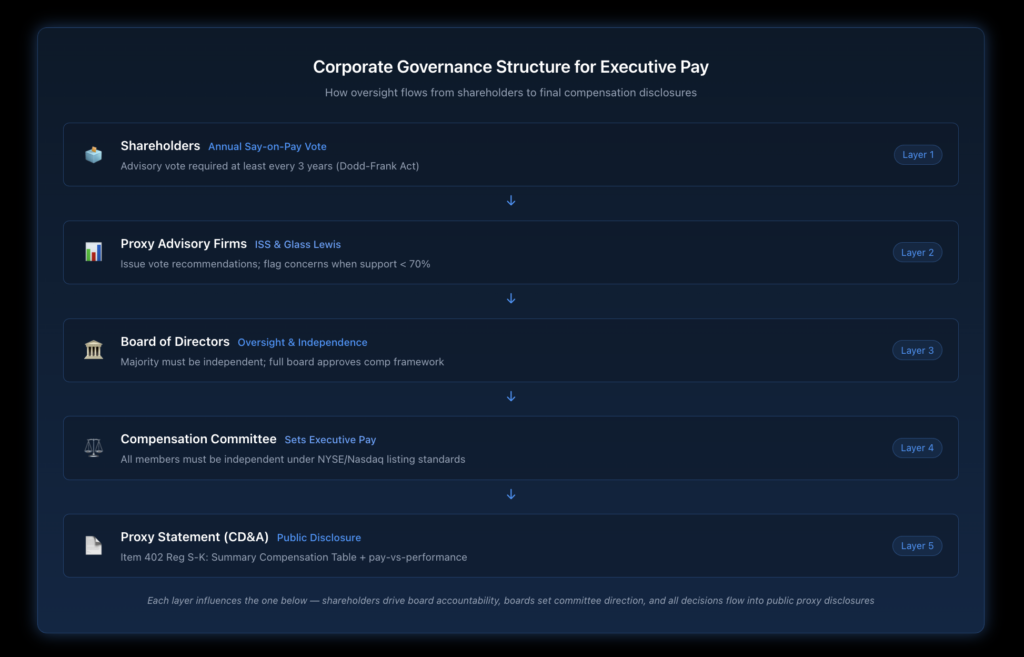

What Is the Role of the Board in Setting Executive Pay?

The board of directors—not management—is legally responsible for setting executive compensation at publicly traded companies. That sounds simple enough, but the process involves layers of oversight, independence standards, and regulatory requirements that executives need to understand.

Who Actually Makes Pay Decisions?

At most public companies, the compensation committee handles executive pay. Under NYSE Section 303A listing standards, compensation committee members must be independent directors—meaning they can’t have a material relationship with the company that would compromise their judgment. That independence requirement was tightened by the Dodd-Frank Act, and the SEC formally codified it under Rule 10C-1.

The compensation committee typically handles:

- Base salary determinations for the CEO and other named executive officers (NEOs)

- Annual bonus plan designs and targets

- Long-term equity award grants

- Severance and change-in-control protections

- Peer benchmarking against comparable companies

What Is the Compensation Discussion & Analysis?

The Compensation Discussion & Analysis, or CD&A, is the narrative section of the annual proxy statement where companies explain pay decisions in their own words. Under Item 402 of Regulation S-K, the CD&A must cover why each element of pay was chosen, how targets were set, and whether the board considered the results of recent say-on-pay votes.

For executives, the CD&A is where your pay philosophy is explained publicly. A well-written CD&A can justify packages that might otherwise draw shareholder criticism. A poorly written one can spark proxy advisor opposition even when the underlying pay is reasonable.

What Is Say-on-Pay and Why Does It Matter to Executives?

Say-on-pay is the shareholders’ advisory vote on executive compensation—and it’s the most visible governance tool investors have for expressing approval or disapproval of how top leaders are paid.

How Does Say-on-Pay Work?

Under Section 951 of the Dodd-Frank Act, all public companies must include a say-on-pay vote in their annual shareholder meeting materials at least once every three years. Shareholders cast an advisory, non-binding vote to approve or disapprove the compensation of the company’s named executive officers.

The vote is advisory—the board isn’t legally required to change anything if shareholders vote against. But in practice, a low vote triggers significant governance scrutiny.

What Happens When Say-on-Pay Fails?

The proxy advisory firm ISS flags say-on-pay votes with less than 70% approval as requiring a meaningful board response. If the compensation committee doesn’t credibly address shareholder concerns in the following proxy cycle, ISS may recommend voting against compensation committee members themselves. That kind of escalation is something most boards—and the executives they oversee—want to avoid.

When say-on-pay support drops substantially, companies typically respond by:

- Increasing shareholder engagement and outreach

- Modifying pay structures, particularly equity award sizing

- Improving disclosure transparency in the CD&A

- Reducing or eliminating problematic pay practices like excessive perks or excise tax gross-ups

From an executive’s perspective, this dynamic means your compensation is never entirely private. The structure, rationale, and alignment with performance are all visible to institutional investors and their advisors. Review our executive compensation guide for a broader overview of how these elements fit together.

How Does Proxy Disclosure Work, and What Must Be Revealed?

Proxy disclosures are far more detailed than most executives realize. Federal securities law requires public companies to lay out CEO pay and the compensation of other top earners in considerable detail each year.

What Gets Disclosed in the Proxy Statement?

The Summary Compensation Table lists total annual compensation for the CEO, CFO, and at least three other most highly compensated executive officers. This includes salary, bonus, equity compensation, non-equity incentive plan compensation, pension value changes, and all other compensation.

Under the SEC’s pay-versus-performance rule, effective for fiscal years ending December 16, 2022, or later, companies must also disclose how “executive compensation actually paid” relates to the company’s financial performance over a multi-year period, including total shareholder return, peer group TSR, and net income. This newer requirement is designed to give shareholders clearer tools for evaluating whether pay aligns with results.

What Are Named Executive Officers Required to Disclose?

Named executive officers—the CEO, CFO, and the three to four other most highly compensated executives—have their pay disclosed in detail every year. If your total compensation lands you in that group, your salary, bonus, equity grants, and other pay are in the public record.

This is worth understanding as you negotiate your own package. Elements like deferred compensation arrangements, perquisites, and change-in-control provisions all show up in the proxy. Structures that look reasonable in context can draw negative attention if disclosed without proper explanation. In situations where governance disclosures relate to internal compliance matters, executives should also be aware of whistleblower protections that may apply.

How Do Proxy Advisory Firms Influence Executive Pay?

Proxy advisory firms—primarily ISS (Institutional Shareholder Services) and Glass Lewis—review executive compensation programs at thousands of companies and issue vote recommendations to institutional shareholders. Their influence over say-on-pay outcomes is substantial.

What Is ISS’s Pay-for-Performance Framework?

ISS applies a quantitative pay-for-performance screening that compares a company’s executive compensation to peer group pay, then evaluates whether pay aligns with shareholder returns over one-year and three-year periods. When ISS finds a significant misalignment, it recommends that shareholders vote against the say-on-pay proposal. Their compensation policies are updated annually and published publicly at issgovernance.com.

Factors that commonly generate negative ISS recommendations include:

- CEO pay that significantly exceeds peer compensation without corresponding performance

- Excessive discretionary bonuses that override formulaic plan results

- Single-trigger change-in-control severance payments

- Excise tax gross-ups on severance

- Repricing of underwater stock options without shareholder approval

- Non-GAAP adjustments that materially inflate incentive payouts without clear disclosure

For performance-based compensation structures specifically, ISS looks for transparent goal disclosure, rigorous target-setting, and a clear rationale for any mid-cycle adjustments.

Does Proxy Advisor Opposition Always Affect Voting Outcomes?

Not always—some institutional investors follow their own governance frameworks rather than deferring to ISS or Glass Lewis. But large institutional holders like index funds often default to proxy advisor recommendations, particularly on routine matters.

The practical reality is that a negative ISS recommendation can shift enough institutional votes to produce meaningful opposition. For a company with a concentrated base of retail shareholders, that might not matter much. For companies with large institutional ownership—common in New York’s financial and professional services sectors—a negative recommendation carries real weight.

Understanding this ecosystem helps executives anticipate how their compensation structures might be evaluated before the proxy season arrives. Negotiating executive employment agreements with an eye toward proxy advisor guidelines can reduce the risk of governance-driven complications later.

What Are the Key Governance Practices That Protect Executives?

Good corporate governance isn’t just a constraint on executive pay—it’s also a framework that can protect executives when properly structured.

How Do Clawback Provisions Interact with Governance?

Under SEC compensation committee listing standards, companies listed on national exchanges must adopt clawback provisions that require recoupment of erroneously paid incentive compensation following a financial restatement. NYSE and Nasdaq listing standards require these policies to cover all current and former executive officers.

Beyond the regulatory minimum, ISS and Glass Lewis have increasingly pushed for broader clawback policies that address misconduct, reputational harm, and risk management failures—not just accounting restatements. If your company’s clawback policy is narrower than what proxy advisors consider adequate, that can factor into say-on-pay recommendations.

For executives, understanding the specific triggers in your company’s clawback policy matters. The board compensation committee typically has discretion over enforcement, and that discretion has limits—but also flexibility—depending on how the policy is written.

How Do Change-in-Control Provisions Fit into the Governance Picture?

Change-in-control provisions and golden parachutes draw consistent scrutiny from governance watchdogs. The Dodd-Frank Act added a requirement for a separate shareholder advisory vote to approve golden parachute arrangements when a company solicits votes for a merger or acquisition.

Proxy advisors look unfavorably at:

- Single-trigger vesting acceleration (where equity vests simply upon a change of control, without termination)

- Excise tax gross-up payments under Section 280G

- Excessive cash severance multiples

- Extended non-compete restrictions coupled with reduced severance

Well-structured change-in-control protections—typically double-trigger vesting, reasonable cash severance caps, and no excise tax gross-ups—tend to pass governance scrutiny while still providing meaningful protection.

What Should New York Executives Know About Governance and Pay Disputes?

New York executives operate in one of the most heavily regulated employment environments in the country. Federal disclosure requirements under the Securities Exchange Act layer onto state contract law protections, and New York courts have developed a substantial body of employment law around executive pay disputes.

What Happens When Governance Processes Lead to Pay Disputes?

Sometimes the governance process itself becomes the basis for a pay dispute. Compensation decisions made without proper board authority, in violation of committee independence requirements, or in breach of an executive’s employment agreement can all be challenged.

In New York, executive compensation disputes often arise around:

- Discretionary bonus denials after a compensation committee decision to eliminate or reduce bonuses

- Clawback enforcement that may exceed what the employment agreement permits

- Post-termination pay obligations when the manner of termination triggers severance under the agreement

- Executive severance and retirement disputes when the company characterizes a departure differently than the executive does

- Equity compensation vesting disputes when employment ends during a performance period

New York courts generally honor the specific terms of executive employment contracts over general claims of breach. This makes it critical for executives to negotiate clear, detailed agreements that address what happens if the compensation committee changes course. Executives who face adverse treatment after raising concerns about pay practices may also have retaliation protections worth exploring.

How Does Shareholder Influence Affect Executive Employment Agreements?

Institutional shareholders have become more active in challenging pay structures they view as excessive, and that pressure can lead to mid-cycle changes in how companies interpret or enforce executive pay arrangements. If your agreement allows the compensation committee to exercise discretion over bonuses, for example, governance-driven board decisions to reduce payouts can be hard to challenge without express contractual protections.

One area that deserves specific attention is golden parachute provisions. Because these are now subject to separate shareholder disclosure and advisory vote requirements in connection with mergers, their structure is more visible—and more scrutinized—than standard severance terms. Building them with governance standards in mind, not just financial calculations, tends to produce more durable arrangements. Executives navigating corporate transitions may also want to review the severance negotiation guide for context on how separation packages interact with employment agreement rights.

Ready to Protect Your Executive Compensation Interests?

Corporate governance rules around executive pay are complex, and they interact directly with your employment agreement, your equity awards, and your rights in the event of a departure or corporate transaction. Whether you’re negotiating a new package, navigating a clawback dispute, or trying to understand how a pending merger affects your compensation protections, having experienced legal counsel on your side matters.

Nisar Law Group represents executives across New York and New Jersey in employment and compensation disputes. Our attorneys understand both the legal framework and the practical governance realities that shape executive pay outcomes. Contact us today for a consultation to discuss your situation.

Frequently Asked Questions About Corporate Governance and Executive Compensation

A say-on-pay vote is a non-binding shareholder advisory vote on the compensation paid to a company’s named executive officers, required at least once every three years under the Dodd-Frank Act. While the vote doesn’t legally require the board to take specific action, companies with significant opposition votes typically face pressure from proxy advisors, institutional shareholders, and governance watchdogs to address the concerns raised. Failure to respond meaningfully can result in adverse recommendations against compensation committee members in subsequent proxy cycles.

Public companies must include a Compensation Discussion & Analysis explaining pay philosophy and decisions, a Summary Compensation Table showing total compensation for each named executive officer, and various supporting tables covering equity awards, options, pension benefits, and other pay elements. Since December 2022, companies must also include pay-versus-performance disclosure showing how executive pay tracks against financial metrics,s including total shareholder return, net income, and a company-selected measure over a multi-year period.

Under NYSE and Nasdaq listing standards—strengthened by SEC Rule 10C-1 under the Dodd-Frank Act—compensation committee members must be independent directors free of any material relationship with the company. The rules require consideration of the source of any consulting or advisory fees paid to the director, and whether the director is affiliated with the company or a related entity. Controlled companies and smaller reporting companies are exempt from some requirements.

Firms like ISS and Glass Lewis analyze thousands of executive pay programs and issue vote recommendations to institutional shareholders ahead of annual meetings. Their pay-for-performance frameworks evaluate whether CEO pay aligns with shareholder returns relative to peer companies. A negative say-on-pay recommendation can shift meaningful institutional vote blocks, and persistent low support levels can trigger escalation to votes against compensation committee members themselves.

Change-in-control provisions are subject to heightened scrutiny from proxy advisors and shareholders. Single-trigger vesting acceleration, excise tax gross-ups, and excessive cash severance multiples are consistently viewed as problematic governance practices that can generate opposition in say-on-pay votes. Executives are generally better protected by double-trigger provisions that require both a change in control and an adverse employment action, coupled with severance terms that fall within market standards rather than outlier amounts.

Yes. Under SEC rules implementing the Dodd-Frank Act, listed companies must adopt clawback policies that allow recoupment of incentive compensation paid during the three years before a financial restatement, regardless of whether the executive was responsible for the restatement. Broader discretionary clawback policies—covering misconduct or reputational harm—may allow recovery of compensation paid even before the policy was adopted, depending on how the policy is written. Executives should review their company’s clawback policy carefully when negotiating any compensation arrangement.