Equity compensation gives executives an ownership stake in the company they work for, tying part of their pay to the business’s long-term success. The most common types include stock options (both incentive and non-qualified), restricted stock units (RSUs), restricted stock awards, performance shares, and employee stock ownership plans (ESOPs). Each type carries different vesting rules, tax treatment, and risk profiles—and understanding these differences is critical before you sign an employment agreement or negotiate a compensation package.

Key Takeaways

- Stock options give you the right to purchase shares at a set price, but incentive stock options (ISOs) and non-qualified stock options (NSOs) are taxed very differently.

- RSUs are among the most common equity awards today because they retain value even if the stock price drops below the grant price.

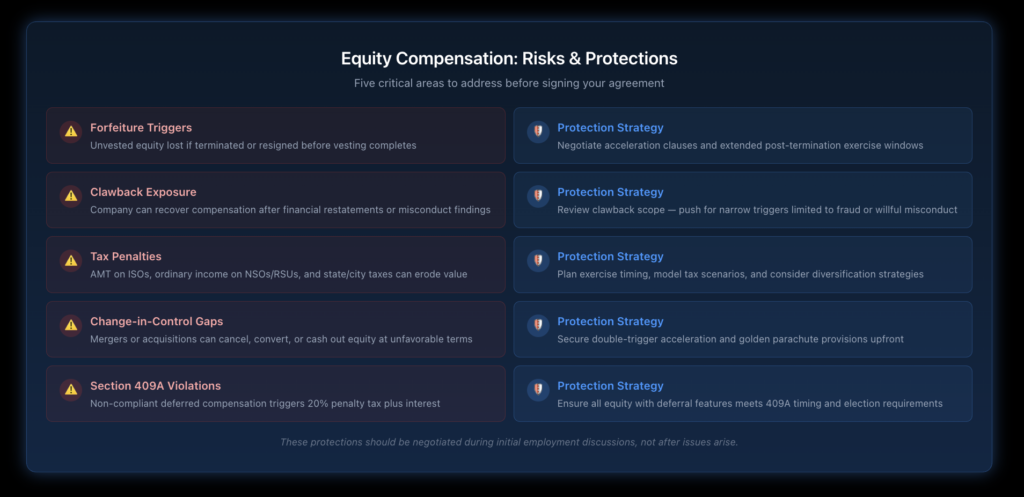

- Vesting schedules determine when you actually own your equity—leaving before vesting means forfeiting unvested shares.

- Section 409A compliance affects nearly all deferred compensation arrangements, and violations trigger a 20% penalty tax plus interest.

- New York imposes state and local taxes on equity compensation, which can significantly reduce your net proceeds.

- An employment attorney can review your equity package to identify hidden risks in clawback provisions, forfeiture clauses, and change-in-control terms.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

How Do Stock Options Work for Executives?

Stock options are one of the oldest forms of equity compensation. They give you the right to buy company shares at a predetermined price (the “exercise price” or “strike price”) after meeting certain conditions, usually a vesting period.

The value comes from the spread—the difference between what you pay to exercise and what the shares are actually worth. If your strike price is $50 and the stock trades at $80, each option is worth $30 before taxes.

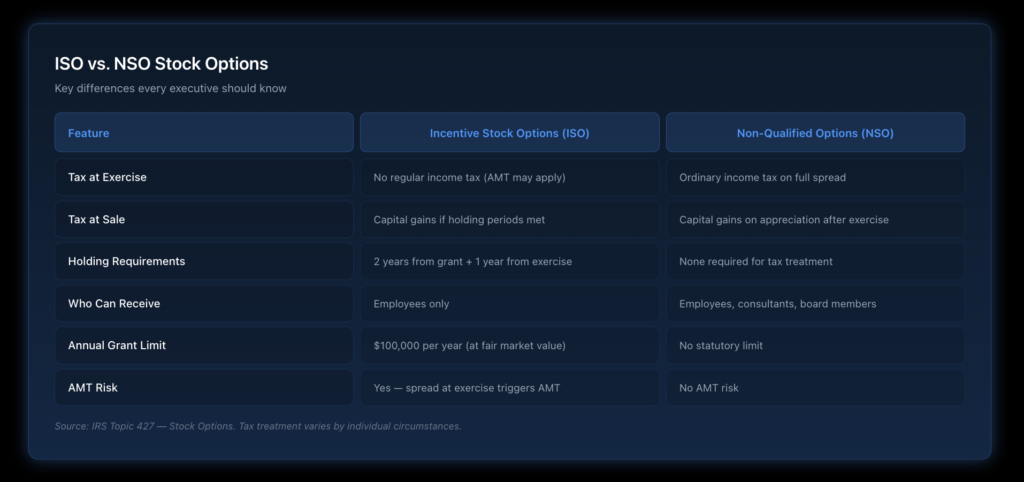

What Is the Difference Between ISOs and NSOs?

The two main categories are incentive stock options and non-qualified stock options, and the tax consequences are dramatically different. ISOs receive favourable capital gains treatment if you meet specific holding requirements—you must hold the shares for at least two years from the grant date and one year from the exercise date. According to IRS guidance on stock option taxation, ISOs are not taxed at exercise for regular income tax purposes, though they can trigger Alternative Minimum Tax (AMT) liability.

NSOs, on the other hand, are taxed as ordinary income at exercise on the full spread between the exercise price and fair market value. Your employer withholds income and payroll taxes at the time of exercise. NSOs offer less favourable tax treatment but come with fewer restrictions—they can be granted to consultants, board members, and other non-employees.

When Should You Exercise Your Stock Options?

Timing matters more than most executives realise. Early exercise strategies can reduce AMT exposure for ISOs, while waiting to exercise NSOs in a lower-income year can minimise your overall tax burden. The decision depends on your financial situation, the company’s stock trajectory, and your executive employment agreement terms.

What Are Restricted Stock Units and How Do They Differ from Restricted Stock?

RSUs have become the dominant equity vehicle at publicly traded companies. An RSU is a promise to deliver shares (or their cash equivalent) once vesting conditions are met. You don’t own any actual shares until vesting occurs, which means you have no voting rights or dividends during the waiting period.

Restricted stock awards work differently. You receive actual shares at grant, but they’re subject to forfeiture restrictions. You own the shares from day one, which means you can vote and receive dividends—but you’ll lose them if you leave before the restrictions lapse.

How Does Vesting Affect Your Equity Compensation?

Vesting schedules are the mechanism that determines when you actually gain full ownership of your equity. The two most common structures are time-based vesting (typically four years with a one-year cliff) and performance-based vesting tied to hitting specific business targets.

Understanding your vesting schedule is essential when evaluating any offer. If you leave a company halfway through a four-year vest, you could walk away from a substantial amount of money. This is why negotiating your executive employment terms should include careful attention to acceleration clauses—particularly change-in-control provisions that can trigger full or partial vesting if the company is acquired.

Can You Make a Section 83(b) Election for Restricted Stock?

If you receive restricted stock (not RSUs), you have the option to file a Section 83(b) election with the IRS within 30 days of the grant. This election lets you pay ordinary income tax on the value of the shares at grant—which may be very low for early-stage companies—rather than at vesting when the shares could be worth significantly more.

The risk is real, though. If you file an 83(b) election and later forfeit the shares because you don’t meet vesting requirements, you can’t get that tax payment back. This decision requires careful analysis with both a tax advisor and an employment attorney who understands performance-based compensation structures.

What Are the Tax Implications of Equity Compensation?

Tax planning is arguably the most important part of managing equity compensation. The wrong move can cost you tens of thousands of dollars—or more.

How Is Equity Compensation Taxed at the Federal Level?

The federal tax treatment depends entirely on the type of equity you hold. RSUs are taxed as ordinary income when they vest, based on the fair market value of the shares on the vesting date. NSOs are taxed as ordinary income at exercise. ISOs receive preferential treatment, but can trigger AMT if you hold the shares past the calendar year of exercise.

For executives with deferred compensation arrangements, Section 409A of the Internal Revenue Code adds another layer of complexity. This provision governs when deferred compensation can be paid and imposes severe penalties for noncompliance—a 20% additional tax plus an interest penalty. Compliance with 409A requirements should be built into every executive compensation arrangement from the start.

What About New York State and City Taxes on Equity Compensation?

New York executives face some of the highest combined tax burdens on equity compensation in the country. The state applies its own rules for sourcing equity income, and the New York State Department of Taxation and Finance has specific guidance on how stock option income is allocated for tax purposes.

If you worked in New York during part of the vesting or service period, a portion of your equity income will be taxable by New York regardless of where you live when the options vest or are exercised. New York City residents face an additional local income tax layer on top of federal and state obligations.

What Role Do ESOPs Play in Executive Compensation?

Employee Stock Ownership Plans are tax-qualified retirement plans that invest primarily in employer stock. According to the NationalCentrer for Employee Ownership, ESOPs cover roughly 14 million participants across American companies.

ESOPs offer unique tax advantages. Company contributions to an ESOP are tax-deductible, and employees don’t pay tax on the shares until they receive distributions. The IRS provides specific guidance on ESOP qualification requirements and distribution rules. A Congressional Research Service analysis has noted that ESOPs serve as both a retirement benefit and a corporate finance tool.

For executives, ESOPs interact with other compensation elements in important ways. They’re governed by ERISA regulations that impose fiduciary duties on plan administrators, and board compensation committees need to ensure ESOP transactions occur at fair market value.

How Can You Protect the Value of Your Equity Compensation?

What Should You Look for in Clawback Provisions?

Clawback provisions allow companies to recover compensation already paid to executives under certain circumstances—financial restatements, misconduct, or violation of restrictive covenants. The SEC’s executive compensation disclosure rules require public companies to maintain and disclose clawback policies.

Review every clawback clause carefully. Some are narrowly tailored to fraud or restatement scenarios, while others are broad enough to capture routine performance shortfalls. The difference can mean hundreds of thousands of dollars.

What Happens to Your Equity During a Corporate Transaction?

Mergers, acquisitions, and other corporate events can dramatically affect the value and timing of your equity compensation. Golden parachute provisions and change-in-control terms in your agreement determine whether your unvested equity accelerates, converts to acquirer stock, or is cashed out.

Without proper protections negotiated upfront, you could find yourself with underwater options or forfeited RSUs after a deal closes. According to recent SEC reporting requirements, public companies now must disclose detailed pay-versus-performance comparisons, giving executives better visibility into how their compensation stacks up.

Why Should Executives Negotiate Severance Protections for Equity?

One of the most overlooked aspects of equity compensation is what happens when you leave the company—whether voluntarily or not. Most equity plans give you a narrow window (often 90 days) to exercise vested options after termination, and unvested awards are typically forfeited entirely.

Executives going through severance negotiations should push for extended exercise periods, accelerated vesting of a portion of unvested equity, and clear treatment of equity in wrongful termination scenarios. Planning for eventual executive severance and retirement should be part of every equity compensation conversation from day one. These protections are much easier to secure during initial hiring negotiations than after a separation has already begun.

Need Help Evaluating Your Equity Compensation Package?

Equity compensation is one of the most valuable—and most complex—parts of executive pay. Getting it right requires understanding the tax rules, negotiating protective contract terms, and planning ahead for corporate events that could impact your awards. Nisar Law Group’s employment attorneys help executives across New York and New Jersey evaluate, negotiate, and protect their equity compensation. Contact us today for a consultation to discuss your specific situation.

Frequently Asked Questions About Equity Compensation

Equity compensation is a form of non-cash pay that gives employees or executives an ownership interest in the company. It typically includes stock options, restricted stock units, restricted stock awards, performance shares, and employee stock ownership plans. The goal is to align the employee’s financial interests with the company’s long-term success, incentivising them to contribute to business growth. Equity compensation is especially common in executive packages, tech startups, and publicly traded companies looking to attract and retain top talent.

Yes, equity compensation is generally treated as taxable income, though the timing and type of tax depend on the specific award. RSUs are taxed as ordinary income when they vest. Non-qualified stock options are taxed at exercise. Incentive stock options receive preferential capital gains treatment if holding period requirements are met, but may trigger AMT liability. The key takeaway is that every form of equity compensation eventually results in a tax obligation, so planning ahead is essential.

The biggest risks include concentration of your wealth in a single company’s stock, forfeiture of unvested awards if you leave early, complex tax obligations that can catch you off guard, and illiquidity—especially at private companies where there’s no public market for the shares. Clawback provisions can also require you to return compensation you’ve already received. Understanding these risks before accepting an equity-heavy package is critical.

Equity compensation can be extremely valuable when it’s structured properly, and the company performs well. It offers upside potential that cash compensation alone can’t match, and it provides favourable tax treatment in certain structures. However, equity is only as good as the company’s stock performance, and concentration risk means you’re heavily exposed to a single asset. The best approach is to treat equity as one part of a diversified financial strategy, not a guaranteed payout.

The reporting method depends on the type of equity. RSU income typically appears on your W-2 in the year of vesting. NSO spread at exercise is also reported on your W-2. For ISOs, your employer reports the exercise on Form 3921, and you may need to calculate AMT adjustments on Form 6251. When you eventually sell the underlying shares, capital gains or losses are reported on Schedule D and Form 8949. Keeping detailed records of grant dates, exercise dates, and cost basis is essential for accurate reporting.

ESOPs and 401(k) plans serve different purposes. An ESOP invests primarily in employer stock and is funded by the company, while a 401(k) typically offers diversified investment options funded by employee contributions with an optional employer match. ESOPs provide tax-free growth and can offer significant upside if the company performs well, but they carry concentration risk. Many companies offer both plans, giving employees retirement diversification alongside ownership incentives.

Start by understanding every detail of your equity agreement—the vesting schedule, exercise windows, tax treatment, and what happens at termination or during a corporate transaction. Work with a tax advisor to plan exercise and sale timing strategically. Negotiate protective terms upfront, including acceleration clauses and extended post-termination exercise periods. Diversify your portfolio over time rather than holding all your wealth in company stock, and keep meticulous records for tax reporting purposes.