Clawback provisions are contractual or regulatory mechanisms that allow employers to recoup previously paid compensation from executives under certain triggering conditions. If you’re an executive or senior leader at a publicly traded company, these provisions almost certainly apply to you — and understanding them is critical to protecting your financial interests. Since the SEC’s Rule 10D-1 took effect in October 2023, every company listed on a U.S. securities exchange must maintain a mandatory clawback policy. That means your bonuses, stock awards, and other incentive compensation could be subject to recovery even if you did nothing wrong.

Key Takeaways

- Mandatory clawback policies now apply to all publicly traded companies under SEC Rule 10D-1, requiring recovery of erroneously awarded incentive compensation after financial restatements.

- Clawbacks can apply even without personal fault — if your company restates its financials, your incentive compensation may be recovered regardless of your involvement in the error.

- The three-year lookback period means incentive compensation received in the three fiscal years before a restatement determination can be clawed back.

- New York’s employment laws create additional considerations for executives, including wage protection rules that may limit certain types of clawback enforcement.

- Negotiating clawback terms in your employment agreement is one of the most important steps you can take to protect your compensation.

- Both regulatory and contractual clawbacks exist — and many companies maintain policies that go well beyond the SEC’s minimum requirements.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

What Types of Clawback Provisions Should Executives Know About?

Two broad categories of clawback provisions affect executive compensation, and the distinction matters significantly for how you protect yourself.

What Are Regulatory Clawback Requirements?

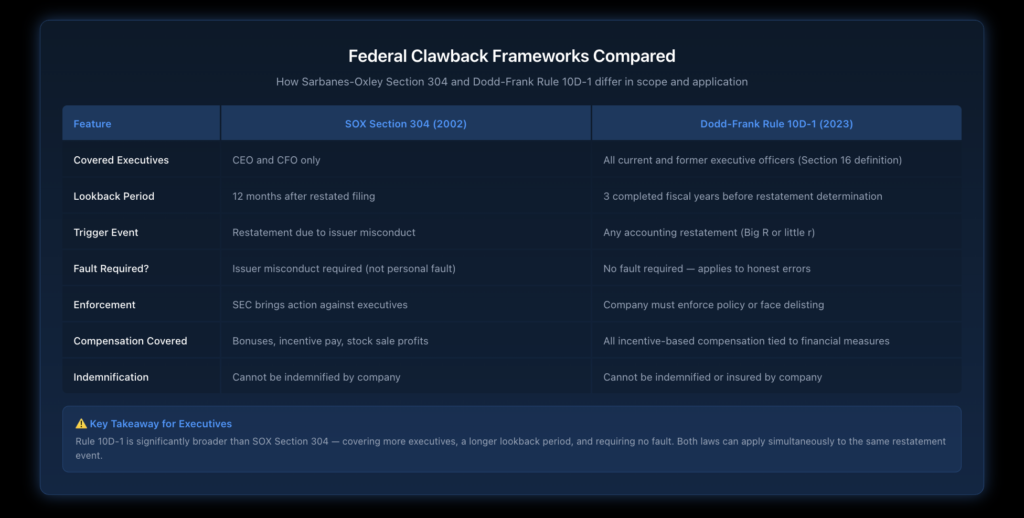

Regulatory clawbacks are mandated by law and apply regardless of what your employment agreement says. The two primary federal frameworks are the Sarbanes-Oxley Act Section 304 and the Dodd-Frank Act’s Section 10D, implemented through SEC Rule 10D-1.

Under Sarbanes-Oxley Section 304, CEOs and CFOs must reimburse their companies for bonuses and stock sale profits received during the 12 months following a financial filing that’s later restated due to misconduct. The critical point here is that courts have consistently held this applies even when the CEO or CFO wasn’t personally involved in the misconduct.

The Dodd-Frank clawback rule is even broader. It applies to all current and former executive officers — not just CEOs and CFOs — and covers a three-year lookback period preceding a restatement. Unlike Sarbanes-Oxley, it doesn’t require any misconduct at all. A simple accounting error that requires a restatement can trigger mandatory recovery.

What Are Contractual Clawback Provisions?

Beyond regulatory mandates, many companies include additional clawback provisions in employment agreements, equity award plans, and performance-based compensation structures. These contractual provisions often go well beyond what the SEC requires.

According to research from the Harvard Law School Forum on Corporate Governance, 80% of large-cap companies maintain expanded clawback policies that exceed the SEC’s minimum requirements. Common expanded triggers include executive misconduct unrelated to financial restatements, violations of non-compete or non-solicitation agreements, breaches of fiduciary duty, and reputational harm to the company.

These broader provisions are typically discretionary, meaning the board or compensation committee decides whether to invoke them. That discretion can work for or against you, depending on the circumstances.

What Events Trigger a Clawback?

Understanding what activates a clawback is essential for assessing your risk exposure. The triggers vary depending on whether you’re dealing with regulatory or contractual provisions.

What Triggers an SEC-Mandated Clawback?

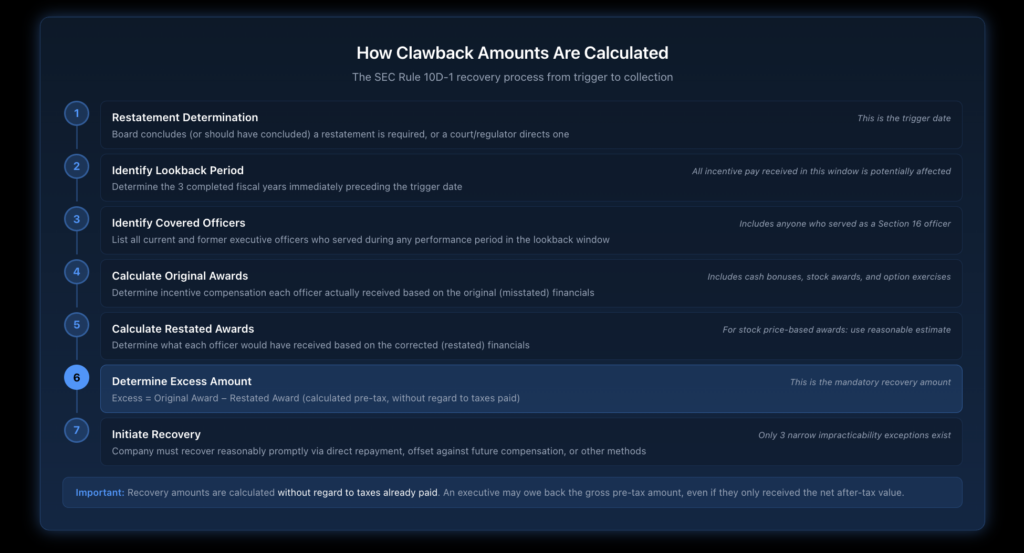

Under Rule 10D-1, a clawback is triggered when a company determines it must prepare an accounting restatement due to material noncompliance with financial reporting requirements. This includes both “Big R” restatements (material errors that require refiling previous financials) and “little r” restatements (errors that are corrected in the current period).

The trigger date is the earlier of when the board concludes a restatement is required or when a court or regulator directs a restatement. Once triggered, the company must recover the excess — the difference between what was paid and what should have been paid based on the restated financials.

What Are Common Contractual Clawback Triggers?

Contractual clawback provisions in your executive employment agreement may include additional triggers such as termination for cause, violation of restrictive covenants, material breach of company policies, ethical violations or compliance failures, and conduct that results in significant financial or reputational harm.

Some companies also include clawback provisions tied to specific change in control scenarios or when executives receive payments based on performance metrics that are later determined to have been inaccurately measured.

How Is Clawback Compensation Calculated?

The calculation method depends on the type of clawback and the compensation involved.

How Does the SEC Calculate Recovery Amounts?

For incentive compensation based on financial reporting measures like revenue or earnings, the calculation is relatively straightforward. The company determines what would have been paid under the restated financials and recovers the excess. For equity compensation tied to stock price or total shareholder return, companies must use a “reasonable estimate” of the effect of the restatement on the applicable measure. This creates more room for dispute, and the company must document its methodology.

The recovery amount is calculated without regard to taxes paid by the executive. That means you could owe back the gross amount even though you only received the net after-tax value — a potentially devastating financial impact.

What Compensation Is Subject to Clawback?

Under Rule 10D-1, “incentive-based compensation” includes any compensation granted, earned, or vested based in whole or in part on the attainment of a financial reporting measure. This covers cash bonuses tied to financial performance, stock options, and restricted stock units with performance conditions, annual and long-term incentive plan payouts, and any other compensation where the grant or vesting depends on meeting financial targets.

Base salary, time-vested equity awards without performance conditions, and truly discretionary bonuses not tied to financial metrics are generally not covered by the SEC’s mandatory clawback rules.

How Does New York Law Affect Clawback Enforcement?

For executives working in New York, state employment law creates an additional layer of complexity around clawback enforcement that’s important to understand.

What Protections Does New York Labor Law Provide?

New York has strong wage protection statutes that can limit an employer’s ability to recoup certain types of compensation. Under New York Labor Law, employers generally cannot make deductions from wages without proper written authorization. The key question is whether the compensation being clawed back qualifies as “wages.”

New York courts have drawn important distinctions here. Incentive compensation, such as stock options, is generally not considered “wages” under New York law. However, once a discretionary bonus has actually been paid, it may be treated as earned wages, making recovery more difficult for the employer.

How Does the Trapped at Work Act Impact Clawback Provisions?

New York’s Trapped at Work Act, which took effect in December 2025, prohibits employers from requiring “employment promissory notes” as a condition of employment. While the Act primarily targets training reimbursement agreements, it includes exceptions for repayment of sums advanced to employees and agreements tied to specific performance benchmarks.

Executives should have their employment agreements reviewed to ensure clawback provisions comply with this new law. The interaction between federal SEC requirements and New York’s evolving employment legislation creates situations where careful legal analysis is essential.

What Is the Faithless Servant Doctrine?

New York also recognizes the “faithless servant” doctrine, which gives employers a powerful tool to recover compensation from employees who engaged in disloyal conduct. Under this doctrine, an employer can potentially claw back all compensation paid during the period of disloyalty — not just the compensation tied to the specific misconduct. This is particularly relevant for executives because the scope of recovery can be significantly broader than what federal clawback rules require.

How Can Executives Negotiate Better Clawback Terms?

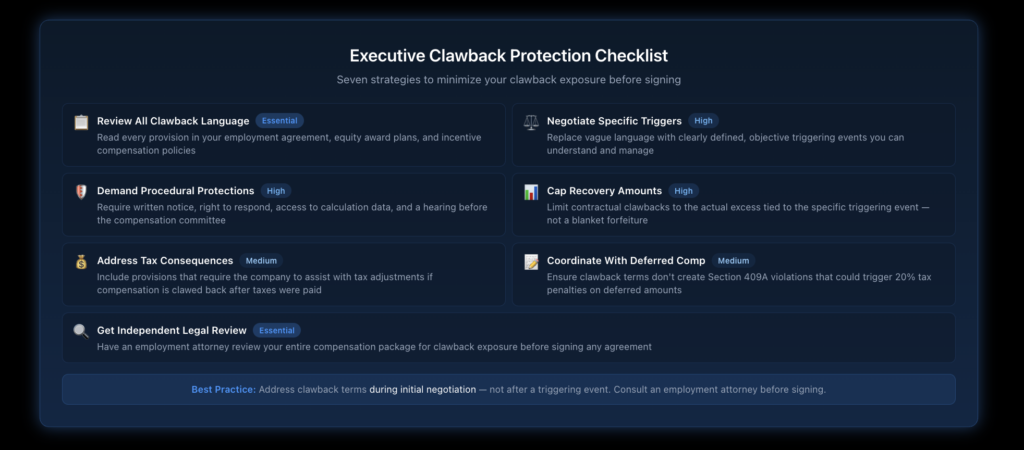

One of the most effective ways to manage clawback risk is to negotiate favorable terms before you accept a position. The time to address clawback exposure is during the initial executive compensation negotiation, not after a triggering event occurs.

What Clawback Terms Should You Negotiate?

There are several provisions you can push for during employment agreement negotiations. First, seek clear definitions of triggering events. Vague language like “conduct detrimental to the company” gives the employer broad discretion. Push for specific, objective triggers that you can understand and manage.

Second, negotiate caps on recovery amounts. While you can’t override federal regulatory requirements, you can limit the scope of contractual clawback provisions. Request that any recovery be limited to the actual excess compensation tied to the specific issue — not a broader forfeiture of all incentive pay.

Third, include procedural protections. Your agreement should require written notice before any clawback is initiated, an opportunity to be heard by the board compensation committee, a reasonable timeframe to respond to clawback demands, and access to the calculation methodology and supporting data.

How Can You Protect Your Deferred Compensation?

Executives with significant deferred compensation arrangements should pay particular attention to how clawback provisions interact with Section 409A compliance requirements. If a clawback reduces or cancels deferred amounts, it could trigger Section 409A penalties if not properly structured.

Work with counsel to ensure that any clawback provisions in your compensation arrangements are drafted in a way that maintains 409A compliance. This often requires specific language about the timing and method of recovery.

What Should You Do If You Receive a Clawback Demand?

If your employer initiates a clawback action against you, the steps you take in the first few days can significantly affect the outcome.

What Are Your Immediate Rights?

Don’t agree to any repayment without first reviewing the specific terms of the clawback provision being invoked, whether the triggering event actually satisfies the contractual or regulatory requirements, the accuracy of the calculation methodology, whether any exceptions or defenses apply, and the statute of limitations for enforcement. New York has a six-year statute of limitations on contract claims, which is relevant for contractual clawback enforcement.

When Should You Challenge a Clawback?

There are legitimate grounds to challenge certain clawback demands. Under Rule 10D-1, companies can forgo recovery when the direct cost of enforcement exceeds the amount to be recovered, when recovery would violate home country law adopted before November 2022, or when recovery would cause a tax-qualified retirement plan to fail to meet Internal Revenue Code requirements.

For contractual clawbacks, potential defenses include disputing whether the triggering event actually occurred, challenging the calculation of the recovery amount, arguing that the provision is unconscionable or unenforceable under applicable law, and raising procedural failures in the clawback process.

How Do Clawbacks Interact With Severance and Exit Planning?

For executives planning a departure or negotiating severance arrangements, clawback provisions can create significant complications. It’s critical to understand your continuing exposure even after you leave the company.

How Long Do Clawback Obligations Last After Departure?

Under Rule 10D-1, the lookback period covers the three completed fiscal years immediately preceding a restatement determination date. If you received incentive compensation during that window, it remains subject to clawback even after you’ve left the company. Contractual clawback provisions may have their own survival periods that extend well beyond your employment. Review the specific terms to understand the full duration of your exposure.

What About Clawbacks and Golden Parachute Payments?

Golden parachute payments triggered by change in control events can also be subject to clawback if they include incentive-based compensation tied to financial reporting measures. When negotiating exit terms during a transaction, make sure to address how existing clawback obligations interact with your parachute payments and ensure that the acquiring company’s clawback policies don’t create additional exposure beyond what you originally agreed to.

Understanding the relationship between corporate governance standards and compensation recovery requirements is essential for any executive navigating a corporate transaction.

Ready to Protect Your Executive Compensation?

If you’re an executive facing a clawback demand, negotiating employment terms with clawback provisions, or planning a departure that involves complex compensation recovery issues, Nisar Law Group can help. Our employment law attorneys have extensive experience advising executives across New York and New Jersey on compensation protection strategies. Contact us today for a consultation to discuss your specific situation.

Frequently Asked Questions About Clawback Provisions

Clawback provisions are terms in employment agreements or regulatory requirements that allow companies to recover previously paid compensation from executives. They’re most commonly triggered by financial restatements, executive misconduct, or violations of employment agreement terms. Under the SEC’s Rule 10D-1, all publicly traded companies must now maintain mandatory clawback policies that apply to incentive-based compensation received in the three fiscal years before a restatement.

Yes, clawback provisions are generally enforceable when properly drafted and executed. Federal regulatory clawbacks under the Dodd-Frank Act and Sarbanes-Oxley Act carry the force of law and cannot be waived by the employer or employee. Contractual clawbacks must meet basic contract law requirements — clear terms, adequate consideration, and compliance with applicable state wage and hour laws. New York courts will enforce reasonable clawback provisions but may scrutinize overly broad or ambiguous terms.

A company can require you to return a bonus under certain circumstances, particularly if the bonus was tied to financial performance metrics that were later found to be inaccurate due to a restatement. For publicly traded companies, SEC Rule 10D-1 makes this mandatory when a restatement occurs. For private companies, the ability to claw back a bonus depends on the specific terms of your employment agreement and applicable state law. In New York, once a bonus has been paid, it may be treated as earned wages, creating additional hurdles for the employer.

A catch-up clause and a clawback provision work in opposite directions. A catch-up clause allows an executive to receive additional compensation to make up for amounts they missed or were shorted under a particular arrangement — commonly seen in carried interest or profit-sharing structures. A clawback provision, by contrast, allows the employer to take back compensation that was already paid. While catch-up clauses add money to the executive’s pocket, clawback provisions remove it.

The most common triggers include financial restatements (required under SEC rules), executive misconduct such as fraud or ethical violations, violations of non-compete or non-solicitation agreements, termination for cause, and breaches of fiduciary duty. Under SEC Rule 10D-1, the trigger is specifically an accounting restatement, and fault isn’t required. Contractual clawback triggers vary by agreement and often include broader events like reputational harm or compliance failures.

Clawback risk refers to the possibility that compensation you’ve already received could be recovered by your employer at a future date. This risk is particularly significant for executives with large portions of compensation tied to company financial performance. The risk extends for at least three years under SEC rules, and potentially longer under contractual provisions. Executives can manage this risk through careful agreement negotiation, maintaining personal financial reserves, and obtaining independent legal review of compensation arrangements.

The SEC’s Rule 10D-1, which became effective in October 2023, requires all companies listed on U.S. securities exchanges to adopt written clawback policies. These policies must provide for the recovery of erroneously awarded incentive-based compensation from current and former executive officers following any accounting restatement. The rule applies regardless of fault, covers a three-year lookback period, and companies face delisting if they fail to comply. Additionally, New York’s Trapped at Work Act adds state-level considerations for certain types of compensation recovery provisions.

The 2.5-month rule is a tax timing concept under IRS regulations, not a clawback rule. It provides that certain bonus payments made within two and a half months after the end of the fiscal year in which they were earned can avoid being treated as deferred compensation under Section 409A. This is relevant to clawback discussions because if a bonus paid within this window is later clawed back, it can create complex tax consequences. Executives should coordinate with tax advisors to understand the interaction between clawback recovery and applicable tax rules.