If you’re an executive or key employee with deferred compensation, Section 409A of the Internal Revenue Code controls almost everything about when and how you get paid. Violating its rules—even unintentionally—can trigger immediate taxation of your entire deferred balance, a 20% penalty tax, and premium interest charges. These penalties fall on you, the employee, not your employer. Understanding how 409A works isn’t optional; it’s the difference between preserving your compensation and losing a significant portion of it to avoidable taxes.

Key Takeaways

- Section 409A governs virtually all nonqualified deferred compensation arrangements, imposing strict rules on deferral elections, distribution timing, and plan documentation.

- Noncompliance penalties include immediate taxation of all vested deferred amounts, a 20% additional tax, and premium interest—all imposed on the employee.

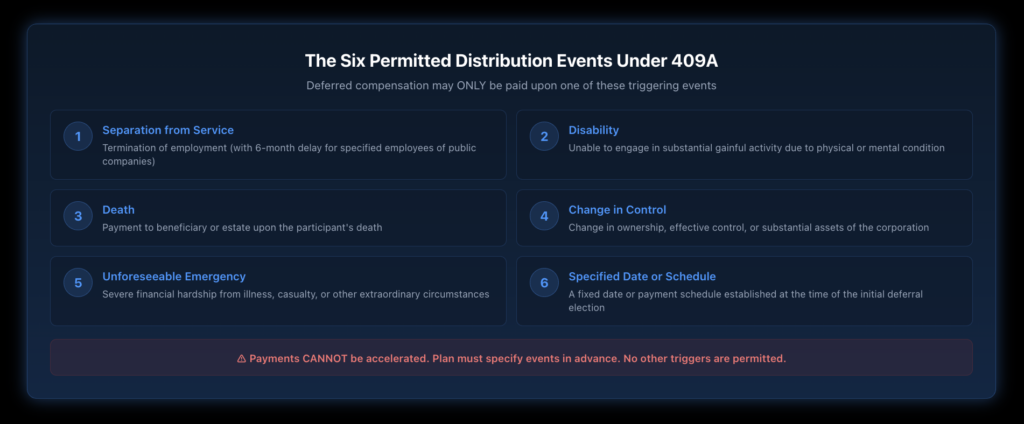

- Only six specific events can trigger payment under a 409A-compliant plan: separation from service, disability, death, change in control, unforeseeable emergency, or a specified date.

- Deferral elections must generally be made before the start of the year in which compensation is earned—changing your mind later is extremely limited.

- The IRS does offer correction programs for inadvertent violations, but the window to act is narrow, and the process is demanding.

- Executives at publicly traded companies face an additional six-month delay on payments triggered by leaving the company.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

What Exactly Is Section 409A and Why Does It Matter?

Section 409A was added to the Internal Revenue Code in 2004 through the American Jobs Creation Act, largely in response to the Enron scandal. Enron executives had accelerated payments from their deferred compensation plans before the company collapsed, walking away with millions while employees lost their retirement savings. Congress responded by creating a rigid framework governing how deferred compensation plans must operate.

The scope of 409A is remarkably broad. It applies to any arrangement where an employee has a legally binding right during one tax year to compensation that may be payable in a later tax year. That includes not just traditional deferred compensation plans, but potentially severance agreements, equity compensation arrangements, bonus plans, and even some employment contract provisions.

Who Does Section 409A Apply To?

409A applies to “service providers”—a category that extends beyond W-2 employees. It covers executives, directors, independent contractors, and board members. The IRS final regulations define “service provider” and “service recipient” specifically to capture this broader scope.

The critical thing to understand is that the penalties for noncompliance fall on the service provider—that’s you, the employee or executive—not on the company. Your employer may face withholding and reporting penalties, but the tax hit lands squarely on your personal return.

What Types of Compensation Does 409A Cover?

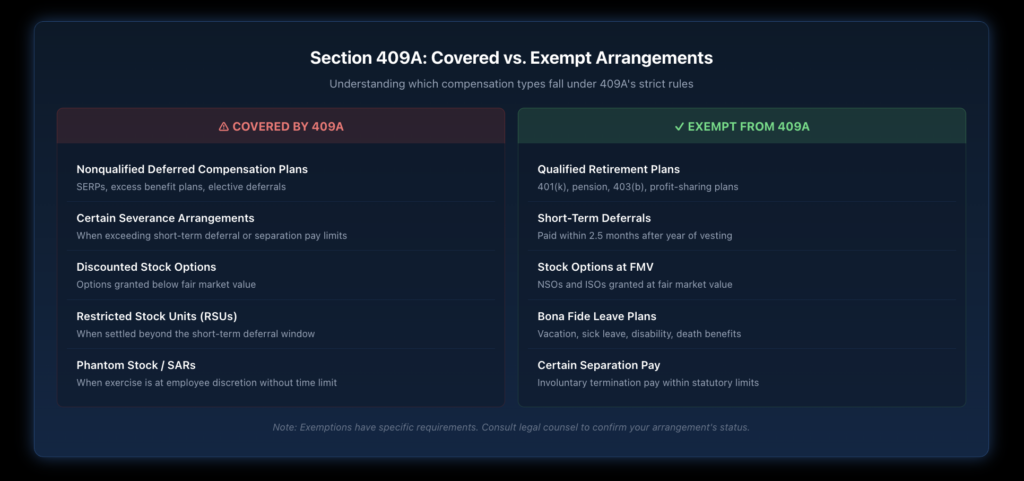

The definition of “nonqualified deferred compensation” under 409A is intentionally expansive. It covers any plan, agreement, or arrangement that provides for the deferral of compensation. However, several important categories are exempt, including qualified retirement plans like 401(k)s and pensions, bona fide vacation and sick leave plans, disability pay, and death benefit plans.

Stock options and stock appreciation rights (SARs) can also be exempt—but only if they’re granted at fair market value and don’t include additional deferral features. This is where 409A valuations become critical for private companies, because undervaluing stock at the time of a grant can turn an exempt option into a 409A violation.

What Are the Core Rules for 409A Deferral Elections?

One of the most important—and most frequently misunderstood—aspects of 409A is the timing of deferral elections. The basic rule is straightforward but unforgiving: you must make your election to defer compensation before the start of the tax year in which you’ll earn it.

When Must Initial Deferral Elections Be Made?

For salary and most forms of compensation, the election deadline is December 31 of the year before the services are performed. If you want to defer a portion of your 2027 salary, you need to make that election by December 31, 2026. Miss the deadline, and you’re out of luck for that year.

There are two notable exceptions. Newly eligible participants get a 30-day window from the date they first become eligible to participate in a plan, though the election only applies to compensation earned after the election date. For performance-based compensation tied to services performed over at least 12 months, the election deadline extends to six months before the end of the performance period.

Can You Change a Deferral Election After It’s Made?

This is where 409A’s rigidity becomes most apparent. Once you’ve made an initial deferral election, the time and form of payment are essentially locked in. Any subsequent change to the payment timing must satisfy strict requirements—most notably, the “five-year rule.”

Under the five-year rule, if you want to push back the payment date, the new payment date must be at least five years later than the original date. You also must make the change at least 12 months before the originally scheduled payment. And the change itself doesn’t take effect for at least 12 months after it’s made. These layered restrictions make it nearly impossible to manipulate payment timing for tax purposes, which is exactly what Congress intended.

What Are the Six Permitted Distribution Events Under 409A?

Section 409A only allows deferred compensation to be paid upon the occurrence of one of six specific triggering events. The plan document must specify which of these events will trigger payment, and payments cannot be accelerated beyond what’s permitted. Those six events are: separation from service, disability, death, a change in control of the corporation, an unforeseeable emergency, or a specified date or fixed schedule.

What Counts as a “Separation from Service”?

This term has a specific technical meaning under 409A that doesn’t always align with what people think of as “leaving a job.” The Treasury Regulations define it based on whether the parties reasonably anticipate that the employee will continue performing services. A reduction in service level to 20% or less of the prior 36-month average creates a presumption of separation.

For key employees of publicly traded companies, there’s an additional wrinkle. If you’re a “specified employee”—generally one of the top 50 officers earning above $150,000—payments triggered by your separation from service must be delayed for six months. This delay is mandatory and must be written into the plan document. Failing to include it is itself a 409A violation.

How Does a Change in Control Trigger Payment?

A change in control can trigger distribution, but only if the event meets 409A’s specific definition. The regulations define three categories: a change in ownership of the corporation, a change in effective control, and a change in ownership of a substantial portion of the corporation’s assets. Each has precise numerical thresholds that must be satisfied.

This matters because many executive employment agreements define “change in control” differently than 409A does. If the plan’s definition is broader than what 409A allows, payments made upon events that don’t qualify under 409A can trigger penalties.

What Happens If You Violate Section 409A?

The penalties for 409A noncompliance are deliberately severe—Congress designed them to be punitive enough to force compliance. When a violation occurs, three things happen to the affected employee.

First, all compensation deferred under the plan for the current and all prior taxable years becomes immediately includible in gross income, to the extent it’s vested and not previously taxed. Second, an additional tax equal to 20% of that deferred amount is assessed. Third, an interest penalty is imposed at the IRS underpayment rate plus 1%, calculated from the year the compensation was originally deferred or vested.

Do Violations Always Affect the Entire Plan?

Here’s what makes 409A particularly dangerous: violations can cascade. Under the plan aggregation rules in the IRS Nonqualified Deferred Compensation Audit Technique Guide, certain types of plans are aggregated for 409A purposes. A violation in one arrangement can contaminate all similar arrangements with the same employer.

For example, all account balance plans from the same employer are treated as a single plan. So a violation in one deferred compensation arrangement could trigger penalties on your entire deferred balance across related plans. This aggregation risk is something many executives don’t realize until it’s too late.

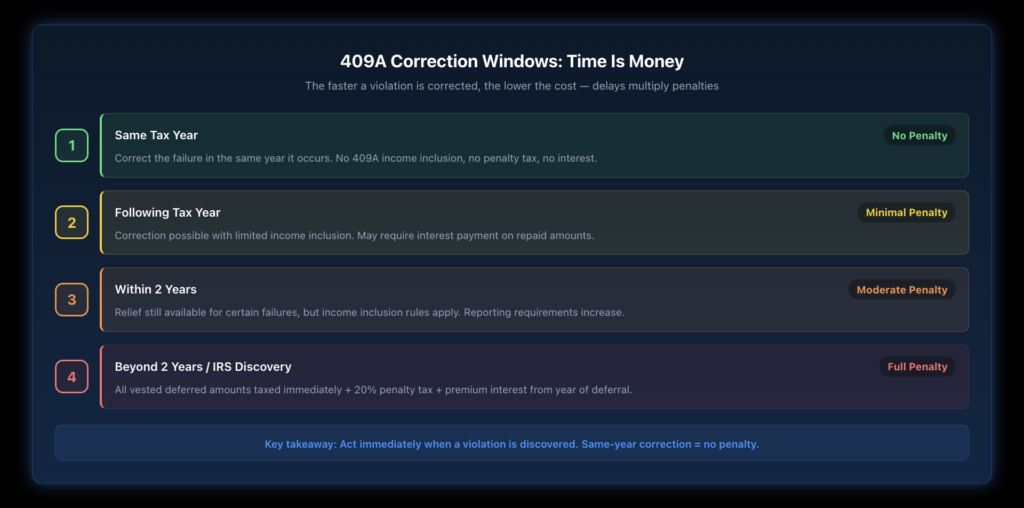

Can 409A Violations Be Corrected?

The IRS has established two main correction programs for inadvertent 409A violations. IRS Notice 2008-113 and Notice 2010-6 provide relief for both operational and document failures. IRS Notice 2008-113 covers operational failures—situations where a compliant plan was administered incorrectly. Notice 2010-6 addresses document failures—where the plan document itself doesn’t comply with 409A requirements.

The key to minimizing damage is speed. If an operational failure is caught and corrected in the same tax year it occurred, there are generally no 409A penalties. Correction in the following year is still possible, but comes with more requirements, including potential interest payments. The longer a violation goes undetected, the more expensive the correction becomes.

How Does Section 409A Interact With Executive Severance Arrangements?

Many severance and retirement packages contain provisions that implicate 409A, and this is one of the most common areas where violations occur. The critical question is whether the severance arrangement constitutes deferred compensation under 409A or falls within an exemption.

What Exemptions Apply to Severance Pay?

There are two main exemptions. The “short-term deferral” rule exempts payments made within 2.5 months after the end of the year in which the right to payment is no longer subject to a substantial risk of forfeiture. The “separation pay” exception covers certain payments made on account of an involuntary separation from service, subject to specific dollar limits and timing requirements.

If neither exemption applies, the severance arrangement is subject to 409A’s full requirements—including the specified employee six-month delay for public company executives. Many severance agreements also require the employee to sign a release of claims before payment, which creates additional 409A timing issues. If the release period straddles two tax years, the plan document must specify when payment will be made to avoid giving the employee control over the tax year of payment.

How Do Release Requirements Create 409A Risk?

Consider this scenario: an executive separates from service in November and has 60 days to sign a release. If they sign in November, payment could be made in the same tax year. If they wait until January, payment occurs in the next tax year. Because the executive effectively controls the timing, this arrangement violates Section 409A unless the plan document addresses the issue.

The standard fix is to include language requiring that payment be made on a specific date (such as the 60th day after separation), regardless of when the release is actually signed. This removes the employee’s ability to control the tax year of payment. Companies negotiating golden parachute or severance provisions need to ensure these timing issues are addressed in the documentation.

What Should Executives Know About 409A and Stock-Based Compensation?

Stock options and other equity awards interact with 409A in ways that can create unexpected problems, particularly for employees of private companies. The general rule is that nonqualified stock options granted at fair market value are exempt from 409A—but “fair market value” has a specific definition under the regulations.

Why Do 409A Valuations Matter for Private Companies?

Publicly traded companies can rely on their stock’s market price. Private companies must use a reasonable valuation method, and the IRS has established safe harbor valuation standards. A “safe harbor” valuation—such as one conducted by a qualified independent appraiser—shifts the burden to the IRS to prove the valuation is “grossly unreasonable” rather than requiring the taxpayer to prove it was correct.

If a stock option is granted below fair market value—even unintentionally—the option becomes subject to 409A as deferred compensation. This can result in the option holder facing the full 409A penalty regime: immediate taxation, 20% penalty tax, and premium interest.

How Do Restricted Stock Units Interact With 409A?

RSUs generally constitute deferred compensation under 409A because the stock isn’t actually transferred until a future date. However, RSUs can qualify for the short-term deferral exemption if the stock is delivered within 2.5 months after the end of the year in which the RSU vests. RSUs that settle later than this window must comply with 409A’s distribution rules.

How Does New York Law Affect Deferred Compensation Arrangements?

New York has its own considerations when it comes to deferred compensation. While 409A is a federal tax provision, executives working in New York also need to think about how state law interacts with their compensation arrangements.

New York State taxes deferred compensation based on where the services were performed when the compensation was earned, not necessarily where you live when it’s paid out. This is particularly relevant for executives who work in New York but plan to retire elsewhere. The New York State Deferred Compensation Board provides oversight of public sector deferred compensation plans, though private sector arrangements are primarily governed by federal law.

Additionally, clawback provisions and corporate governance requirements may affect how deferred compensation is structured and distributed for executives at companies headquartered in or operating within New York. Understanding these overlapping obligations is essential for comprehensive compensation planning.

What Steps Can You Take to Protect Your Deferred Compensation?

Protecting your deferred compensation starts with understanding your plan documents. Every 409A-compliant plan must be in writing, and the document must specify the time and form of payment, the triggering events, and the deferral election procedures. Review these documents carefully—or have an attorney review them—before you sign.

How Can You Audit Your Own 409A Compliance?

Start by confirming that your deferral elections were made on time. Review when your plan says you’ll get paid and verify that the triggering events match 409A’s six permitted categories. Check whether you’re a specified employee subject to the six-month delay. And if your employer has amended your plan or offered you a chance to change your elections, make sure the changes comply with 409A’s modification rules.

If you spot a potential issue, act quickly. The IRS correction programs provide the most favorable treatment for violations corrected within the same tax year. Waiting makes the problem more expensive to fix and could result in the full penalty being imposed.

What Role Does the Compensation Committee Play?

At publicly traded companies, the board compensation committee is responsible for overseeing executive compensation programs, including deferred compensation arrangements. The committee should ensure that plan documents comply with 409A, that operational procedures are in place for proper administration, and that any plan amendments go through proper 409A analysis.

As an executive, you have a right to understand how your compensation committee is managing 409A compliance. Don’t assume it’s being handled correctly—the penalties fall on you, not the committee members.

Ready to Protect Your Deferred Compensation?

If you’re an executive with deferred compensation arrangements, the stakes of getting 409A compliance wrong are too high to leave to chance. Nisar Law Group’s employment law attorneys work with executives across New York and New Jersey to review compensation agreements, identify potential 409A compliance issues, and protect your financial interests. Contact us today for a consultation to discuss your deferred compensation arrangements and ensure you’re fully protected.

Frequently Asked Questions About Deferred Compensation and Section 409A

Section 409A compliance means that a nonqualified deferred compensation plan satisfies the Internal Revenue Code’s requirements for deferral elections, distribution timing, and plan documentation. A compliant plan must be in writing, must specify the time and form of payment using only the six permitted distribution events, and must be operated in accordance with its written terms. Failure to comply with either the plan’s design or its operation triggers immediate taxation of all vested deferred amounts, a 20% penalty tax, and premium interest charges on the affected employee.

The most common violations include making deferral elections after the deadline, accelerating payments outside of the permitted exceptions, paying deferred compensation on events not listed in the six permitted categories, failing to delay payments to specified employees of public companies for six months after separation, and having plan documents that don’t conform to 409A requirements. Both design failures in the plan document and operational failures in administering the plan can trigger penalties.

The five-year rule applies when you want to change the timing of a previously scheduled payment. Under 409A, any subsequent election to delay a payment must push the new payment date at least five years beyond the original date. The change must be made at least 12 months before the originally scheduled payment, and the new election doesn’t take effect for at least 12 months after it’s made. This prevents employees from manipulating payment timing for tax advantages.

The employee or service provider bears the tax burden of 409A noncompliance. When a violation occurs, the deferred amounts become immediately taxable to the employee, who also owes the additional 20% penalty tax and premium interest. The employer faces separate obligations for withholding and reporting, but does not pay the 409A penalty taxes. This makes it critical for employees to independently verify that their deferred compensation arrangements are properly structured.

Under Section 409A, deferred compensation may only be distributed upon one of six specific events: the employee’s separation from service, the employee becoming disabled, the employee’s death, a change in control of the corporation, an unforeseeable emergency, or a date or schedule specified in the plan at the time of the initial deferral election. The plan must designate which events will trigger payment, and distributions cannot be accelerated beyond what these events permit.

The most effective approach is proactive compliance. Make all deferral elections before the applicable deadline, ensure your plan document specifies only permitted distribution events, operate the plan exactly as written, and include the six-month specified employee delay if required. If a violation does occur, use the IRS correction programs as quickly as possible—violations corrected in the same tax year generally avoid penalties entirely. Regular review of plan documents and operations by qualified legal counsel is the best ongoing protection.

Several categories of compensation are specifically exempt from 409A. These include qualified retirement plans like 401(k)s and pensions, bona fide sick leave and vacation plans, disability pay and death benefit plans, certain short-term deferrals paid within 2.5 months after vesting, stock options and SARs granted at fair market value, certain separation pay arrangements for involuntary terminations, and deferrals under Section 457(b) governmental plans. Each exemption has specific requirements that must be satisfied to qualify.