When a company gets acquired, merges with another organization, or undergoes a major ownership shift, executives often find themselves in a vulnerable position. Change in control provisions are contractual safeguards built into employment agreements that protect your compensation, benefits, and job security during these corporate transactions. They define exactly what happens to your pay, equity, and role if the company you work for changes hands—and without them, you could lose significant financial value overnight.

Key Takeaways

- Change in control provisions trigger specific protections when a company experiences a qualifying ownership change, such as a merger, acquisition, or significant board turnover.

- These provisions typically address severance pay, equity acceleration, benefit continuation, and job protection through mechanisms like golden parachutes and double-trigger vesting.

- Single-trigger provisions activate automatically upon a change in control, while double-trigger provisions require both a change in control and a qualifying termination event.

- Section 280G of the Internal Revenue Code imposes a 20% excise tax on excess parachute payments, making tax planning essential.

- New York executives should negotiate these provisions proactively—ideally when first accepting a leadership position, not after a deal is already in motion.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

What Exactly Triggers a "Change in Control"?

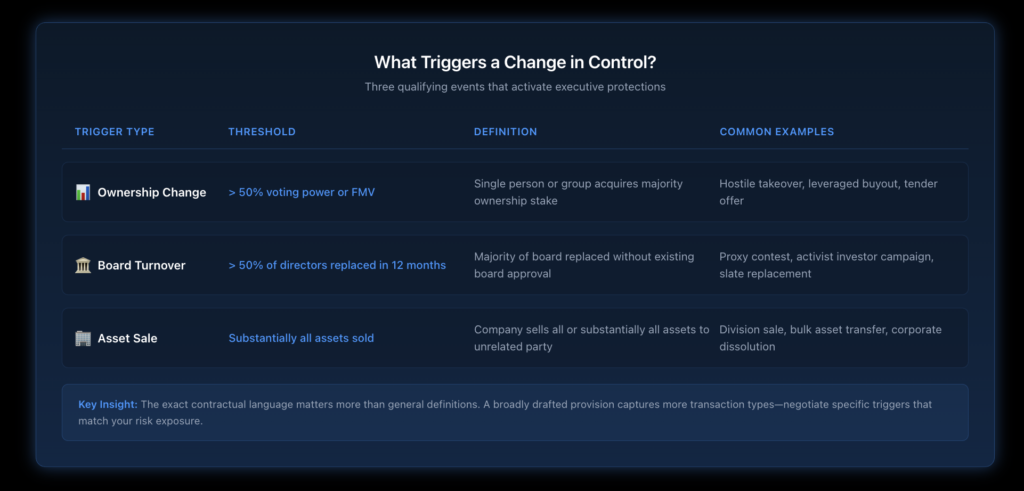

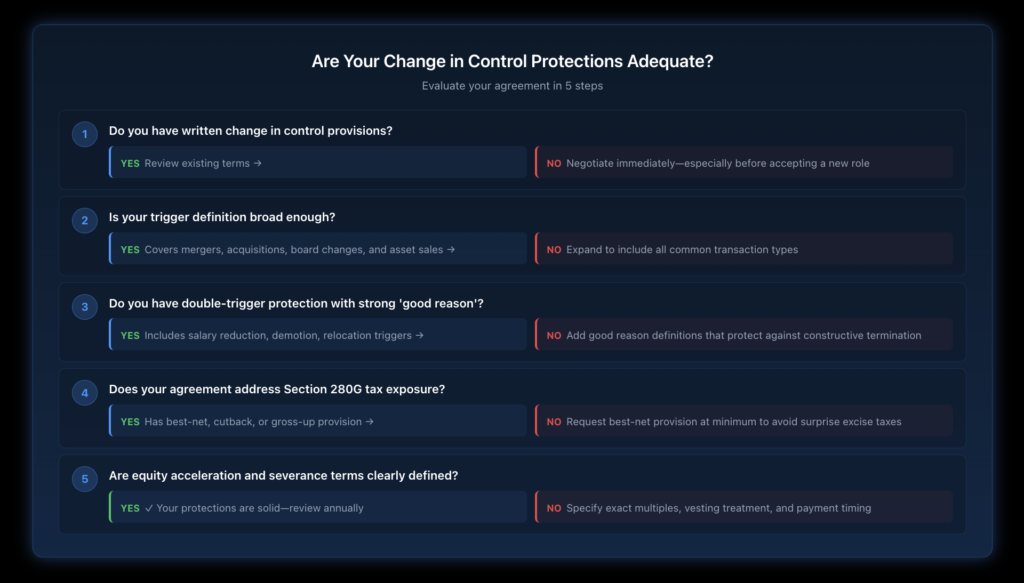

The definition of what constitutes a change in control matters enormously because it determines when your protections actually kick in. Most agreements define a change in control as one or more of the following events.

How Is Ownership Change Defined?

A change in ownership typically occurs when a single person or group acquires more than 50% of the total voting power or fair market value of the corporation’s stock. Under IRS regulations governing golden parachute payments, the threshold focuses on whether someone gains effective control—not just a nominal stake.

Board turnover is another common trigger. If a majority of the board of directors is replaced within a 12-month period without approval from the existing board, that generally qualifies as a change in effective control. Asset sales can also trigger these provisions when a company sells all of its assets substantially to an unrelated party.

Why Does the Specific Definition Matter So Much?

The exact language in your agreement can make a substantial difference. A broadly defined change in control clause might trigger protections during a partial acquisition or a management buyout—situations where a narrowly drafted clause wouldn’t apply at all. Executives who negotiate executive employment agreements should pay close attention to how these triggering events are worded.

What Are Single-Trigger vs. Double-Trigger Provisions?

This is one of the most important distinctions in change in control agreements, and it directly affects when and how your protections activate.

What Happens with Single-Trigger Provisions?

Single-trigger provisions activate immediately upon a change in control event, regardless of whether you keep your job. If your agreement includes single-trigger accelerated vesting, all your unvested stock options and restricted stock units would vest the moment the deal closes—even if you remain employed by the new entity.

The advantage is certainty. You receive your benefits no matter what happens post-transaction. The downside is that companies and shareholders have increasingly pushed back against single-trigger arrangements. Proxy advisory firms like ISS and Glass Lewis routinely recommend voting against compensation plans that include single-trigger equity acceleration because they view these as excessive payouts that don’t require the executive to actually lose anything.

How Do Double-Trigger Provisions Work?

Double-trigger provisions require two events before benefits activate: first, a qualifying change in control, and second, a qualifying termination—typically an involuntary termination without cause or a voluntary resignation for “good reason.” This structure has become the prevailing standard in corporate governance and executive compensation arrangements.

The Dodd-Frank Act’s say-on-pay provisions gave shareholders more influence over executive compensation decisions, and the resulting scrutiny has pushed most public companies toward double-trigger arrangements. For executives, this means the definition of “good reason” becomes critically important. Good reason typically includes material reductions in base salary, authority, or duties; forced relocation beyond a specified distance; or a material breach of the employment agreement by the acquiring company.

What Types of Compensation Are Protected?

Change in control provisions can protect virtually every element of your compensation package. Understanding each component helps you evaluate whether your current protections are adequate.

How Does Severance Pay Work in a Change in Control?

Severance triggered by a change in control is often more generous than standard severance. While typical executive severance and retirement packages might provide six to twelve months of base salary, change in control severance commonly ranges from one to three times the executive’s annual compensation—often defined as base salary plus target bonus.

The payment structure matters too. Lump-sum payments give you immediate access to your money, but they can create significant tax consequences. Installment payments spread the tax burden but carry the risk that the paying entity could default on future obligations.

What Happens to Equity Compensation During a Transaction?

Equity is where the stakes are often highest. Your stock options, restricted stock units, and performance-based compensation awards may be treated very differently depending on what your agreement says.

Common equity protections include accelerated vesting of all unvested awards, conversion of unvested equity into acquiring company shares on equivalent terms, or cash-out of all equity at the transaction price. Without explicit protections, the acquiring company might cancel your unvested equity, assume your awards on less favorable terms, or impose new vesting conditions.

How Are Benefits and Perquisites Handled?

Benefit continuation is another significant element. Change in control provisions often guarantee continued health insurance, life insurance, and disability coverage for a specified period after termination. Some agreements also provide for continued employer contributions to retirement plans or payment of outplacement services.

For executives with substantial deferred compensation balances, protecting those funds during a corporate transaction is essential. Section 409A of the Internal Revenue Code governs the timing of deferred compensation distributions, and a change in control can serve as a permissible distribution event—but only if the plan is properly structured.

What Are the Tax Implications of Change in Control Payments?

Tax planning is not an afterthought—it’s a core part of negotiating effective change in control protections. The penalties for getting this wrong are steep.

How Does Section 280G Affect Golden Parachute Payments?

Section 280G of the Internal Revenue Code targets what it calls “excess parachute payments.” Here’s how it works: if the total value of your change in control payments equals or exceeds three times your “base amount” (essentially your average annual taxable compensation over the prior five years), all payments above one times your base amount become subject to a 20% excise tax under Section 4999. The company also loses its tax deduction for those excess payments.

Consider a practical example. If your base amount is $500,000, the three-times threshold is $1.5 million. If your total change in control payments equal $1.6 million, you won’t just pay excise tax on the $100,000 above the threshold. Instead, the excise tax applies to $1.1 million—everything above your $500,000 base amount. That’s a $220,000 excise tax bill on top of regular income taxes.

What Tax Protection Strategies Should Executives Consider?

There are three main approaches to managing the Section 280G excise tax.

A gross-up provision requires the company to pay an additional amount to cover the excise tax, effectively making the executive whole. These have fallen out of favor due to shareholder criticism, and the Harvard Law School Forum on Corporate Governance has documented their decline in proxy filings.

A cutback provision (sometimes called a “haircut”) reduces your payments to just below the three-times threshold, avoiding the excise tax entirely. This makes sense when the amount you’d lose to the cutback is less than what you’d pay in excise taxes.

A best-net provision compares both scenarios and gives you whichever produces the better after-tax result. This is now the most common approach in executive agreements.

What Should New York Executives Know About Negotiating These Provisions?

Negotiating change in control protections requires strategic thinking and careful timing. New York’s robust employment law framework provides some additional context for these negotiations.

When Is the Best Time to Negotiate?

The strongest negotiating position is before you accept the role, during the initial negotiation of the executive employment agreement process. Once you’re already employed, the company has less incentive to offer generous change-in-control protections. And once a potential deal is on the horizon, negotiating new protections becomes exponentially harder.

That said, certain events create windows for renegotiation: promotions, contract renewals, or significant changes in job responsibilities. The key is to approach these conversations proactively rather than reactively.

What Key Terms Should Be Prioritized?

Focus your negotiation on the provisions that create the most financial impact. The definition of “change in control” should be broad enough to capture the types of transactions most likely to affect your position. The definition of “good reason” in a double-trigger arrangement should include meaningful protections against constructive demotion.

Clawback provisions deserve careful attention, too. Some agreements allow the acquiring company to claw back change in control payments under certain circumstances, which can significantly undermine the protections you’ve negotiated.

Under SEC disclosure requirements, public companies must disclose change in control arrangements in proxy statements, which means your negotiation happens in a somewhat transparent environment. Understanding how board compensation committees evaluate and approve these arrangements can help you frame your requests effectively.

How Does New York Law Affect These Agreements?

New York is a major hub for corporate transactions, and the state’s legal framework shapes how change in control agreements are interpreted and enforced. New York courts generally enforce these agreements as written, placing a premium on clear, specific contract language.

The Department of Labor’s ERISA framework governs certain employee benefit plan aspects that may be affected during corporate transactions. Executives with substantial benefits tied to ERISA-covered plans should ensure their change in control provisions address how those benefits are handled.

New York’s strong public policy favoring employee mobility also comes into play. If your change in control agreement includes non-compete and non-solicitation clauses that become effective upon termination following a change in control, those restrictions may face stricter scrutiny under New York law than in many other jurisdictions.

How Can You Protect Yourself If Your Company Is Being Acquired?

If you’re already in the middle of a potential transaction, there are still steps you can take to protect your interests.

Start by reviewing every compensation-related document you’ve signed—your offer letter, employment agreement, equity award agreements, and any supplemental compensation plans. Identify exactly what protections you currently have and where the gaps exist.

Document your current compensation in detail, including base salary, bonus targets and recent payouts, equity holdings and vesting schedules, deferred compensation balances, and benefit values. This creates a baseline for evaluating any changes the acquiring company proposes.

If your employer asks you to sign new agreements in connection with the transaction, have those documents reviewed by an employment attorney before signing. Acquiring companies sometimes ask executives to waive existing change in control protections in exchange for new arrangements that may be less favorable.

Understanding the golden parachutes tax and regulatory framework is essential for evaluating any proposed modifications to your compensation during a transaction.

Ready to Protect Your Executive Compensation?

If your company is undergoing a change in control—or you want to make sure your employment agreement protects you before one happens—Nisar Law Group can help. Our employment law attorneys work with executives across New York and New Jersey to negotiate, review, and enforce change in control provisions that safeguard your financial interests. Contact us today for a consultation to discuss your specific situation.

Frequently Asked Questions About Change in Control Provisions

A golden parachute is a compensation package that provides substantial financial benefits to an executive when their employment is terminated following a corporate change in control. These packages typically include severance pay, equity acceleration, benefit continuation, and sometimes tax gross-up payments. The term comes from the idea that the executive has a “soft landing” regardless of what happens during the transaction. Section 280G of the Internal Revenue Code imposes special tax rules on golden parachute payments that exceed certain thresholds.

Yes, but your leverage is generally weaker than during initial hiring negotiations. The best opportunities to add or improve change in control protections mid-employment arise during promotions, contract renewals, significant role changes, or when the company is actively trying to retain key talent. If a potential transaction is already rumored, the company may be reluctant to negotiate new protections because doing so increases the cost of the deal.

A change in control involves a fundamental shift in corporate ownership or governance—such as an acquisition, merger, or replacement of a majority of the board. A change in management, by contrast, might simply involve replacing the CEO or other senior leaders without any change in who owns or controls the company. Most change in control provisions are not triggered by mere management changes, which is why the specific contractual definitions matter so much.

Stock options in a change of control can be treated in several ways depending on the agreement terms: accelerated vesting, where all unvested options immediately vest, assumption by the acquiring company where options convert to equivalent awards in the new entity, cash-out where the company pays the difference between the exercise price and the deal price, or cancellation where unvested options are simply terminated. The best outcome for executives is typically full acceleration or a cash-out at favorable terms.

Good reason allows an executive to voluntarily resign and still receive change in control benefits if the employer materially changes the terms of employment after the transaction. Common good reason triggers include a significant reduction in base salary or total compensation, a material diminishment of job title, duties, or reporting relationships, a required relocation beyond a specified distance, or a material breach of the employment agreement by the employer. The specific definition should be carefully negotiated because it determines when you can leave on your own terms and still receive full benefits.

Golden parachute payments are typically approved by the company’s board of directors, often through its compensation committee. For public companies, the Dodd-Frank Act requires a separate non-binding shareholder advisory vote on golden parachute arrangements disclosed in connection with merger or acquisition proxy statements. While this vote is advisory rather than binding, companies pay close attention to shareholder sentiment, and unfavorable votes can influence how aggressively boards approve change in control packages.

Yes, under certain circumstances. The Dodd-Frank Act’s clawback provisions require companies to recover erroneously awarded incentive-based compensation from current and former executive officers. Additionally, individual employment agreements may contain specific clawback provisions that allow recovery of change in control payments if the executive violates non-compete agreements, confidentiality obligations, or other post-employment restrictions. Some agreements also include clawback triggers tied to financial restatements or misconduct discovered after the transaction closes.

Change in control payments are subject to ordinary income tax at applicable federal and state rates. The key additional tax concern is Section 280G, which imposes a 20% excise tax on excess parachute payments when the total change in control compensation equals or exceeds three times the executive’s average annual compensation over the prior five years. The company also loses its tax deduction for excess parachute payments. Deferred compensation triggered by a change in control must also comply with Section 409A timing rules to avoid a separate 20% penalty tax.