Executive compensation packages represent some of the most complex and consequential employment arrangements in the corporate world. Whether you’re a C-suite executive negotiating your first leadership role or a seasoned professional reviewing a renewal offer, understanding the legal framework governing executive pay can mean the difference between a protected career and costly mistakes.

These arrangements go far beyond basic salary negotiations. They involve intricate tax considerations, securities law compliance, and contractual protections that require careful legal analysis. Employment attorneys who specialize in executive compensation help clients navigate everything from equity-based incentives to golden parachute provisions that protect their interests during corporate transitions.

Key Takeaways

- Executive compensation packages typically include five core elements: base salary, annual bonuses, long-term incentives, retirement benefits, and perquisites.

- Tax rules under IRC Sections 409A and 280G impose significant penalties on improperly structured deferred compensation and change-in-control payments.

- Employment agreements should address termination scenarios, non-compete restrictions, and confidentiality obligations before you sign.

- Executives classified as exempt under the FLSA must meet both the salary and duties tests to be excluded from overtime requirements.

- Severance negotiations offer critical opportunities to protect your interests, especially when facing involuntary termination.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

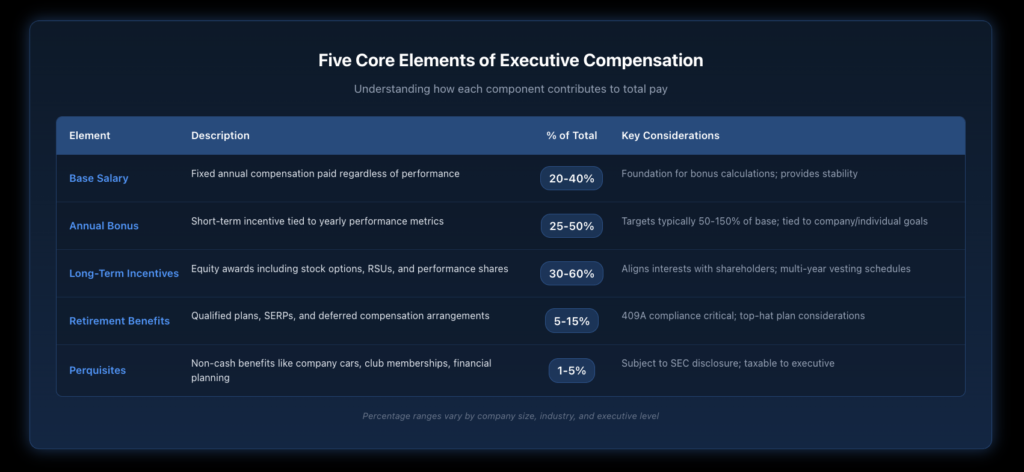

What Are the Five Core Elements of Executive Compensation?

Executive compensation packages typically combine multiple components designed to attract, retain, and motivate senior leadership. Understanding each element helps executives evaluate offers and negotiate effectively.

Base salary provides the fixed foundation of your compensation. For executives at mid-sized companies, base salaries often range from $200,000 to $500,000 annually, while Fortune 500 CEOs may command significantly higher amounts. Your base salary also serves as the calculation basis for many other benefits, making it strategically important beyond its face value.

Annual bonuses tie a portion of your compensation to short-term performance metrics. These performance-based arrangements typically target 50-150% of base salary for senior executives, with actual payouts depending on individual and company performance against predetermined goals.

Long-term incentive plans align executive interests with shareholder value over multi-year periods. Stock options, restricted stock units, and performance shares constitute the most common forms. The Securities and Exchange Commission requires detailed disclosure of executive compensation arrangements in public company filings, providing transparency into how top executives are rewarded.

Retirement and deferred compensation benefits allow executives to accumulate wealth on a tax-advantaged basis. Supplemental executive retirement plans (SERPs) and non-qualified deferred compensation arrangements often extend beyond what 401(k) plans permit, though these programs must comply with strict IRC Section 409A requirements to avoid substantial tax penalties.

Perquisites and benefits round out the package with items like company cars, club memberships, financial planning services, and enhanced insurance coverage. While individually modest compared to other compensation elements, these benefits can add meaningful value and demonstrate the company’s commitment to your personal and professional well-being.

How Do Tax Laws Affect Executive Compensation Structures?

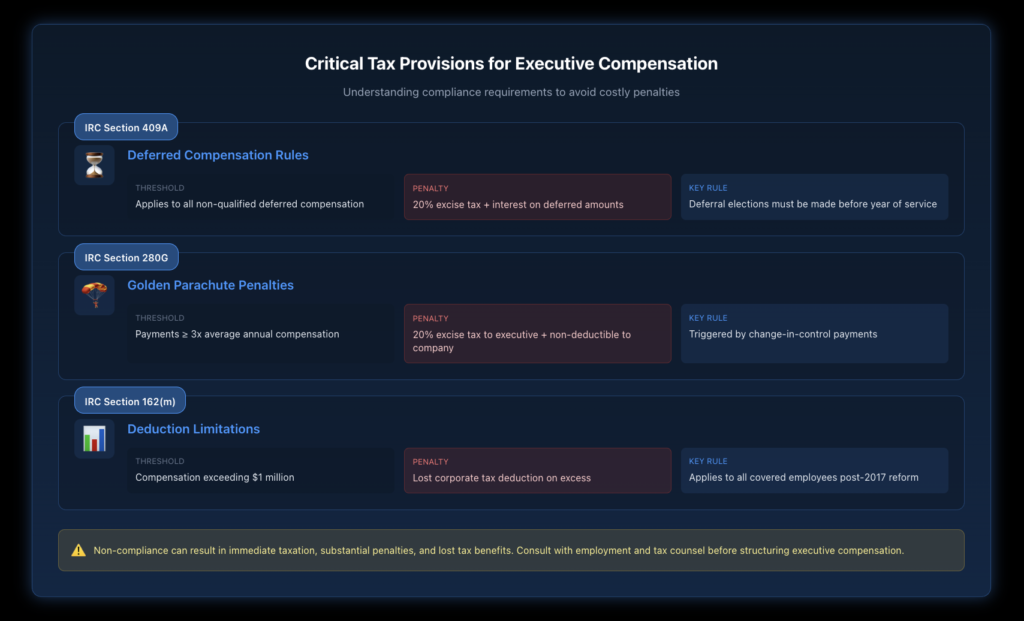

The Internal Revenue Code imposes complex rules on executive compensation that can dramatically affect the after-tax value of your package. Three provisions deserve particular attention.

Section 409A governs non-qualified deferred compensation with strict rules about when compensation can be deferred and when it must be paid. Violations trigger immediate taxation of all deferred amounts plus a 20% penalty tax and interest. Properly structured arrangements must establish deferral elections before the year of service and limit distribution events to specific triggers like separation from service, disability, or a change in control.

Section 280G addresses golden parachute payments made to executives in connection with corporate acquisitions. When an executive’s total change-in-control payments equal or exceed three times their average compensation over the preceding five years, the IRS imposes significant penalties. Excess parachute payments become non-deductible to the corporation and are subject to a 20% excise tax.

The 280G regulations define “parachute payments” broadly to include severance, accelerated equity vesting, and other compensation contingent on a change in control. Private companies can obtain shareholder approval to exempt payments from these penalties, but public companies cannot avoid the rules so easily.

Section 162(m) limits the corporate tax deduction for compensation exceeding $1 million paid to covered employees. Following the 2017 tax reform, this limitation applies to virtually all compensation without the previous exception for performance-based pay.

What Should Your Executive Employment Agreement Include?

A well-drafted executive employment agreement protects both your interests and the company’s legitimate business needs. Several provisions require careful attention.

Term and renewal provisions define the duration of your employment relationship. While some agreements run for specified periods with automatic renewal, others establish at-will arrangements that either party can terminate. The term affects your job security and may influence other provisions like non-compete restrictions.

Duties and reporting relationships should clearly describe your responsibilities and position within the organizational structure. Ambiguity here can lead to disputes about whether the company properly utilized your talents or effectively demoted you without cause.

Compensation terms should memorialize all elements of your package in sufficient detail. For equity compensation, the agreement should reference plan documents that govern vesting schedules, exercise procedures, and treatment upon various termination scenarios.

Termination provisions address what happens when employment ends. Sophisticated agreements distinguish between voluntary resignation, termination for cause, termination without cause, and resignation for good reason. Each scenario may trigger different severance benefits and affect restrictive covenant obligations. Understanding your severance negotiation rights becomes critical when evaluating these terms.

Restrictive covenants, including non-competition, non-solicitation, and confidentiality provisions, can significantly limit your post-employment options. Recent changes in some jurisdictions, including New York, have narrowed the enforceability of non-compete agreements, making it important to understand how local law affects your obligations.

Change-in-control provisions protect executives during corporate transactions. These “double trigger” or “single trigger” arrangements determine whether you receive enhanced benefits automatically upon a deal closing or only if you’re subsequently terminated.

Are You Properly Classified as an Exempt Executive?

The Fair Labor Standards Act exempts certain executive employees from minimum wage and overtime requirements, but only when specific tests are satisfied. Misclassification can expose companies to significant liability and may affect your compensation expectations.

The Department of Labor’s executive exemption requires employees to meet both salary and duties tests. You must be paid on a salary basis at a rate not less than the current threshold, which the DOL periodically adjusts. The Congressional Research Service has documented how these thresholds have evolved over time.

Beyond the salary requirement, exempt executives must perform genuine executive functions. This means your primary duty must be managing the enterprise or a recognized department, you must regularly direct the work of at least two full-time employees, and you must have authority to hire and fire, or your recommendations on personnel matters must carry particular weight.

Highly compensated employees earning total annual compensation above a higher threshold may qualify for exemption under a more relaxed duties test, but they must still customarily and regularly perform at least one exempt duty.

Executives who don’t actually perform management functions—regardless of their job titles or salary levels—may be entitled to overtime compensation. Companies sometimes misclassify managers who spend most of their time performing the same work as their subordinates, which can lead to wrongful termination disputes and wage claims.

How Do Clawback Provisions Work?

Clawback provisions allow companies to recover previously paid compensation under certain circumstances. These provisions have become increasingly common following financial scandals and regulatory reforms.

The Dodd-Frank Act requires public companies to adopt policies for recovering incentive compensation from current and former executives following accounting restatements. Even in the absence of misconduct, if a restatement occurs within three years, companies must claw back excess incentive pay received by executive officers.

Beyond regulatory mandates, many companies include broader clawback provisions in their compensation arrangements. These may permit recovery when an executive engages in conduct detrimental to the company, violates restrictive covenants, or is terminated for cause.

Understanding your clawback exposure helps you evaluate the true risk-adjusted value of incentive compensation and plan accordingly. In some cases, negotiating limitations on clawback provisions may be possible as part of your overall compensation discussion.

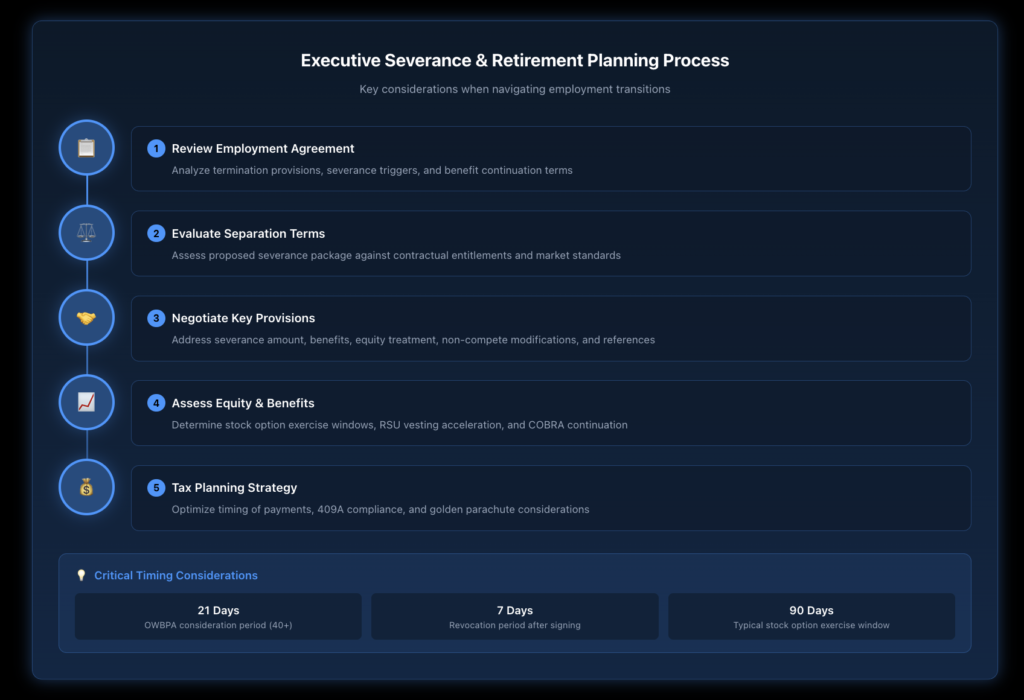

What Governs Executive Retirement and Severance Benefits?

Executive severance and retirement arrangements require careful planning to maximize benefits while minimizing tax consequences. Several legal frameworks apply.

ERISA governs many employee benefit plans, but certain executive arrangements fall outside its requirements. Top-hat plans, which provide deferred compensation to select management employees, enjoy reduced ERISA compliance obligations but still face regulatory constraints.

Non-qualified deferred compensation plans allow executives to defer substantially more compensation than qualified plans permit. However, these arrangements provide less security than qualified plans because the deferred amounts remain subject to the employer’s creditors in bankruptcy.

Rabbi trusts offer some protection by setting aside assets to fund future benefit payments, though the assets remain exposed to corporate creditor claims. Secular trusts provide greater security but trigger immediate taxation, eliminating the deferral benefit.

Supplemental executive retirement plans can guarantee specific benefit levels that exceed qualified plan limits. These arrangements often use formulas based on years of service and final average compensation to calculate benefits.

How Do Board Compensation Committees Oversee Executive Pay?

Compensation committees of corporate boards carry responsibility for designing, implementing, and monitoring executive pay programs. Understanding their role helps executives appreciate how compensation decisions are made.

Stock exchange listing standards require public company compensation committees to consist entirely of independent directors. These committees typically engage compensation consultants to benchmark pay against peer companies and design programs that balance competitive positioning with shareholder interests.

Say-on-pay votes give shareholders an advisory voice on executive compensation. While these votes don’t bind the board, negative results can prompt compensation changes and affect director elections. Companies increasingly engage with major shareholders to understand their compensation concerns.

Compensation committee members face fiduciary duties to the corporation and its shareholders. They must exercise informed business judgment in making compensation decisions and avoid conflicts of interest. Directors who rubber-stamp excessive compensation without appropriate analysis may face personal liability.

What Corporate Governance Issues Affect Executive Compensation?

Executive compensation intersects with corporate governance in ways that affect both disclosure requirements and structural design decisions.

SEC disclosure rules require extensive compensation information in proxy statements. Summary compensation tables, grants of plan-based awards, outstanding equity at fiscal year-end, and potential payments upon termination must all be disclosed. The Grant Thornton analysis of golden parachute rules illustrates how complex these disclosures can become during corporate transactions.

Pay ratio disclosure requires comparison of CEO compensation to median employee pay. While this information may not directly affect your negotiations, it influences public perception of executive compensation and can affect board decision-making.

Institutional investor voting policies increasingly focus on compensation practices. Large shareholders may vote against pay packages they consider excessive, poorly designed, or insufficiently tied to performance. Understanding these perspectives helps executives anticipate how their compensation may be perceived.

Protect Your Executive Compensation Rights

Executive compensation arrangements involve complex legal, tax, and business considerations that can significantly affect your career and financial security. Whether you’re negotiating a new employment agreement, evaluating equity incentives, or facing a termination situation, experienced legal counsel can help protect your interests.

The employment law attorneys at Nisar Law Group have extensive experience representing executives in compensation negotiations, contract disputes, and separation matters throughout New York and New Jersey. We understand both the technical rules governing executive pay and the practical dynamics of these high-stakes negotiations.

Schedule a confidential consultation to discuss your executive compensation questions and learn how we can help you achieve your professional goals while protecting your legal rights.

Frequently Asked Questions About Executive Compensation

Executive compensation encompasses all forms of payment and benefits provided to senior corporate leaders in exchange for their services. The basic structure typically includes base salary as the fixed foundation, annual cash bonuses tied to short-term performance, long-term incentives like stock options or restricted shares, retirement benefits beyond standard 401(k) plans, and perquisites such as company cars or financial planning services. Each component serves different purposes: base salary provides security, bonuses motivate annual performance, equity awards align interests with shareholders over time, and retirement benefits encourage long-term tenure.

The 3 P’s framework—Pay, Performance, and Perquisites—provides a simplified way to categorize executive compensation elements. Pay encompasses fixed components like base salary and guaranteed minimums. Performance covers variable compensation tied to individual or company results, including annual bonuses and long-term incentive awards. Perquisites include non-cash benefits and privileges extended to executives beyond standard employee benefits. Some compensation professionals use an alternative 3 P’s framework focusing on Position, Performance, and Person when determining appropriate pay levels.

When evaluating an executive offer, ask detailed questions about every compensation component. Request clarity on how annual bonus targets are set and what performance metrics determine payouts. Understand the vesting schedule and terms for all equity awards, including what happens to unvested shares upon various termination scenarios. Inquire about severance provisions, change-in-control protections, and any clawback provisions that could require returning previously earned compensation. Ask about non-compete and non-solicitation restrictions that may limit your future employment options. Finally, understand the tax treatment of each compensation element and whether the company provides tax gross-ups for certain payments.

Reasonable compensation depends heavily on company size, industry, geographic location, and executive role. Generally, compensation should be competitive with what similar companies pay executives in comparable positions, appropriately tied to company performance, and designed to attract and retain qualified talent. The IRS may challenge excessive compensation as unreasonable, potentially treating it as a disguised dividend in closely held corporations. Compensation committees at public companies typically benchmark against peer groups and engage independent consultants to establish reasonable pay levels. What’s reasonable for a Fortune 500 CEO differs dramatically from what’s appropriate for a startup executive.

The “70 rule” or similar rules of thumb suggest that executives approaching certain career milestones may receive enhanced severance treatment. One common application provides severance equal to one week of pay for each year of service, with executives whose age plus years of service equals 70 or more receiving additional benefits. However, there is no universal standard, and severance terms vary widely based on individual negotiations, company policies, and industry norms. Employment agreements should clearly specify severance entitlements rather than relying on informal guidelines. Executives should negotiate explicit severance provisions when entering new roles.

Severance pay is taxed as ordinary income, not at a flat 40% rate. However, the effective tax rate on a large severance payment can approach or exceed 40% when combining federal income tax (up to 37%), state and local income taxes, and payroll taxes. Additionally, supplemental wage payments like severance are often subject to mandatory federal withholding at 22% for amounts up to $1 million and 37% for amounts exceeding $1 million. Executives receiving substantial severance should work with tax advisors to understand their actual tax liability and explore strategies for managing the timing and characterization of payments.

Six months’ severance represents a baseline starting point for executive roles but may be inadequate depending on your seniority, tenure, and market conditions. Senior executives often negotiate 12-24 months of severance protection, with some arrangements providing even longer periods. Beyond the duration, consider whether severance includes bonus payments, benefits continuation, equity acceleration, and outplacement services. Severance triggered by termination without cause should typically be more generous than what’s provided upon voluntary resignation. Change-in-control severance often exceeds regular severance to compensate for the uncertainty and risk executives face during corporate transactions.

CEOs who accept $1 salaries typically receive most of their compensation through equity awards rather than cash. This structure aligns the CEO’s interests with shareholders by making compensation dependent on stock price appreciation. Famous examples include Steve Jobs at Apple and Elon Musk at Tesla. However, a $1 salary doesn’t mean minimal compensation—these executives often receive stock options or grants worth millions or billions of dollars. The structure may also provide tax advantages by converting ordinary income into capital gains. Additionally, the gesture carries symbolic value, signaling confidence in the company’s future and willingness to share risk with shareholders.