If you’re an executive navigating a compensation negotiation, understanding how board compensation committees work can make the difference between leaving money on the table and securing the package you deserve. These committees hold enormous influence over how executives are paid — from base salary to long-term equity grants — and the process is far more structured, political, and negotiable than most executives realize.

Key Takeaways

- Board compensation committees are typically composed entirely of independent directors under NYSE and Nasdaq listing standards.

- Committees rely heavily on outside compensation consultants to benchmark pay against peer companies.

- Proxy advisory firms like ISS and Glass Lewis exert significant indirect influence over what committees approve.

- Say-on-pay votes under the Dodd-Frank Act have fundamentally changed how committees approach compensation decisions.

- Executives who understand committee dynamics are better positioned to negotiate favorable packages.

- Legal counsel can help you engage effectively with the process before compensation decisions are finalized.

Disclaimer: This article provides general information for informational purposes only and should not be considered a substitute for legal advice. It is essential to consult with an experienced employment lawyer at our law firm to discuss the specific facts of your case and understand your legal rights and options. This information does not create an attorney-client relationship.

What Is a Board Compensation Committee and What Does It Do?

A board compensation committee is a subcommittee of a company’s board of directors responsible for overseeing and approving executive pay packages. For publicly traded companies listed on the NYSE or Nasdaq, these committees must be composed entirely of independent directors — meaning members who have no material financial relationship with the company beyond their director compensation.

Under NYSE compensation committee requirements, compensation committees are required to have a written charter and consist entirely of independent directors. At a minimum, compensation committees are required to:

- Review and approve goals relevant to CEO compensation

- Evaluate the CEO’s performance against those goals

- Determine and approve CEO compensation based on that evaluation

- Recommend compensation for other senior executive officers

How Are Committee Members Chosen?

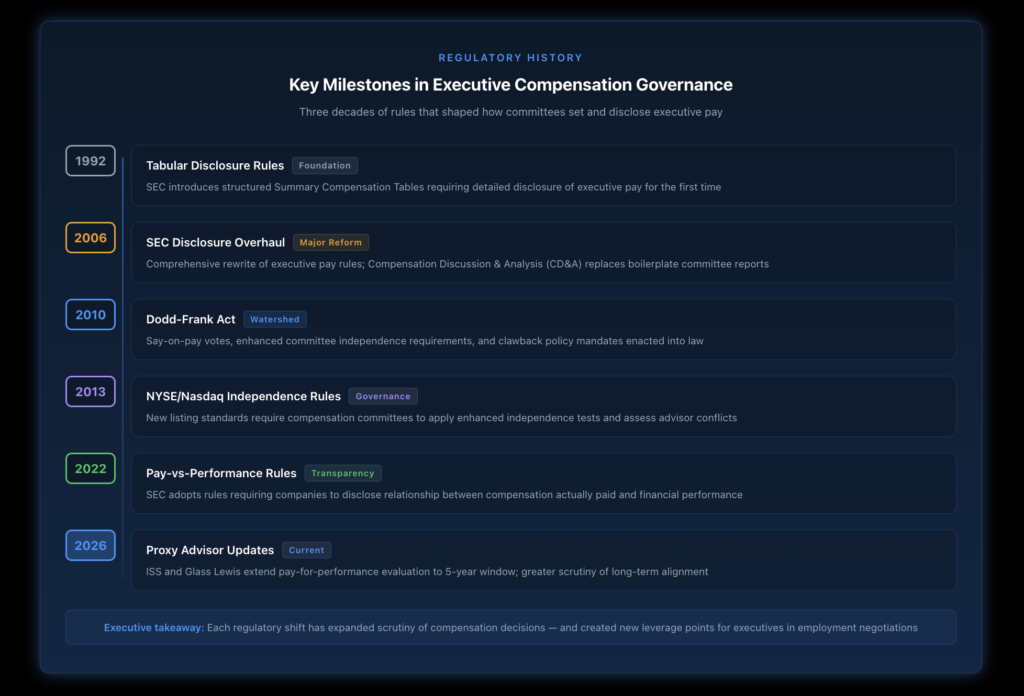

Committee members are independent directors appointed by the full board. Under rules adopted by the NYSE and Nasdaq in response to the Dodd-Frank Act, “independence” for compensation committee purposes goes beyond the standard director independence test. Boards must consider the director’s sources of compensation and any affiliations with the company that might affect their ability to make independent judgments about executive pay.

This enhanced independence standard was designed to ensure that compensation decisions are genuinely arms-length — not shaped by executives who have an interest in how pay decisions turn out.

What Roles Do Compensation Consultants Play?

Most compensation committees retain outside compensation consultants to provide market data, benchmark pay against peer companies, and advise on compensation structure. Before engaging any consultant, the committee must evaluate their independence across six factors specified by SEC rules, including fees paid to the consultant’s firm, other services provided to the company, and personal relationships between the consultant and committee members or senior executives.

It’s worth noting that the committee isn’t required to use an independent consultant — but it must assess independence before taking advice from any advisor. The role of the compensation committee has expanded significantly over the past two decades as shareholder scrutiny of executive pay has intensified.

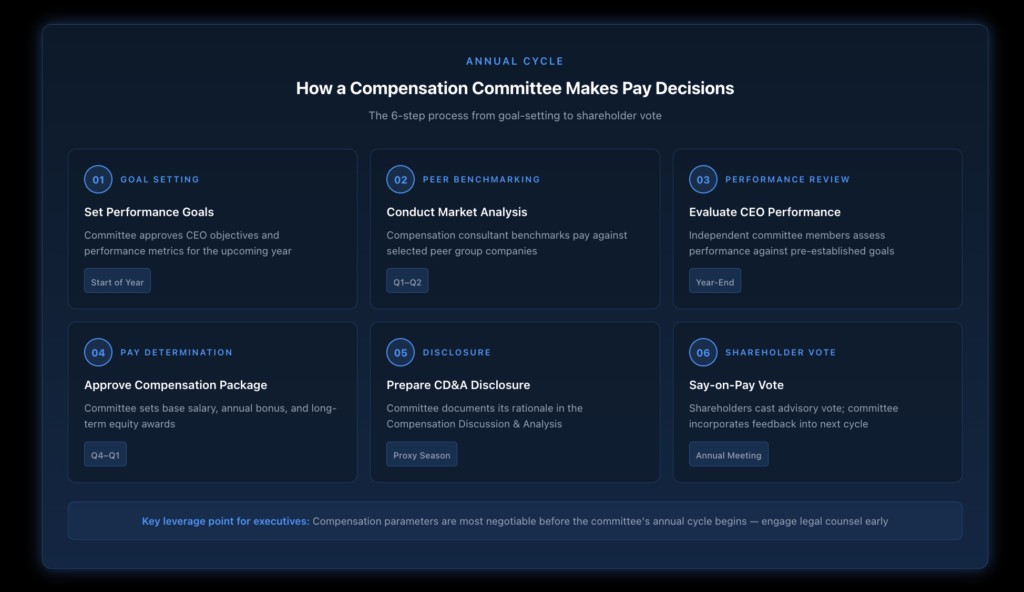

How Do Compensation Committees Actually Set Pay Levels?

The practical process involves several layers of analysis, stakeholder input, and political pressure. Understanding each component helps you anticipate where your negotiating leverage lies.

How Does Peer Benchmarking Work?

Peer group selection is one of the most consequential — and contested — decisions a compensation committee makes. Committees typically target compensation at the 50th to 75th percentile of a peer group, which means the peer group itself determines what “market rate” means.

Peers are usually selected based on industry, revenue size, and market capitalization. But the selection isn’t always objective. Executives sometimes advocate for peer groups that include larger or higher-paying companies, which naturally pulls compensation benchmarks upward.

What Performance Metrics Drive Executive Pay?

Performance-based compensation structures tied to business results are the predominant form of executive pay at public companies today. Committees set targets for metrics like earnings per share, revenue growth, total shareholder return, and increasingly, environmental, social, and governance (ESG) objectives.

The challenge is that performance metrics negotiated before you start a role often become the foundation for every subsequent compensation decision. Committees typically look at whether targets were achievable and whether the executive had genuine influence over the outcomes being measured.

How Does the Committee Handle Discretion vs. Formula?

Most executive pay programs blend formula-driven components (like performance share units tied to specific metrics) with discretionary judgments (like adjustments for extraordinary circumstances). Committees retain discretion to increase or decrease formula-driven awards in light of factors not captured in the metrics.

This discretion cuts both ways. For executives, it can mean the committee recognizes contributions not reflected in the numbers. It can also mean awards get cut in ways that feel arbitrary. Understanding how much discretion exists — and getting it addressed in writing during negotiations — matters significantly.

How Do Say-on-Pay Votes Change What Committees Approve?

The Dodd-Frank Act introduced shareholder advisory votes on executive compensation — commonly called “say-on-pay.” Public companies must hold these votes at least every three years, though most hold them annually, given pressure from institutional investors. The SEC’s say-on-pay framework requires companies to address in their Compensation Discussion & Analysis how they’ve considered the results of the most recent vote.

While say-on-pay votes are non-binding, they have transformed committee behavior. A negative vote — or even a lower-than-expected approval rate — signals shareholder dissatisfaction and can trigger pressure on committee members through director election campaigns.

What Role Do Proxy Advisory Firms Play?

Proxy advisory firms like Institutional Shareholder Services (ISS) and Glass Lewis provide voting recommendations to institutional investors on say-on-pay proposals. Their influence is substantial: a negative recommendation from ISS can shift a significant percentage of the institutional vote, putting compensation decisions under real scrutiny.

Both ISS and Glass Lewis evaluate compensation programs using proprietary pay-for-performance methodologies. ISS recently extended its pay-for-performance evaluation to a five-year time horizon, while Glass Lewis is also moving to a five-year assessment period starting in 2026. Committees increasingly design pay programs with proxy advisor preferences in mind — which shapes what they’re willing to approve.

What Happens After a Failed Say-on-Pay Vote?

Companies that receive low say-on-pay support are expected to engage with shareholders to understand concerns and demonstrate responsiveness in subsequent years. Committees that ignore negative votes risk facing “withhold” campaigns against their members in director elections. This creates a feedback loop where committee decisions are continuously shaped by anticipated shareholder reaction.

For executives, this means compensation packages that deviate significantly from market norms — in terms of structure, pay levels, or performance metrics — may face resistance not because they’re inherently unreasonable, but because they trigger proxy advisor concerns.

What Legal Disclosures Govern Compensation Committee Decisions?

Public companies are required to disclose detailed information about executive compensation under SEC Regulation S-K, Item 402. This disclosure appears in the annual proxy statement and includes:

- A Compensation Discussion & Analysis (CD&A) explaining the principles behind pay decisions

- Summary compensation tables covering the three most recently completed fiscal years

- Grants of plan-based awards and outstanding equity awards

- Pension benefits and nonqualified deferred compensation

The regulatory framework under 17 CFR § 229.402 sets detailed disclosure requirements covering every element of pay for named executive officers. The CD&A is “filed” with the SEC rather than merely furnished, which means misleading statements carry securities law liability.

Under the Harvard Law Forum’s Compensation Committee Guide, committees must meet a comprehensive set of responsibilities that go well beyond simple pay approval.

How Does NYSE Committee Independence Work?

NYSE listing standards under Section 303A require that compensation committees consist entirely of independent directors. In evaluating independence for committee purposes, the board must consider all factors specifically relevant to whether a director has a relationship with the company that is material to their ability to make independent judgments about executive compensation.

The NYSE requires that compensation committee charters address the committee’s authority to retain advisors, the committee’s responsibility for assessing advisor independence, and its responsibility for the appointment, compensation, and oversight of any advisor’s work.

What Is the Compensation Discussion and Analysis?

The CD&A is the narrative heart of executive compensation disclosure. It explains the committee’s objectives, how pay decisions were made, and why specific amounts were approved for each named executive officer. Under Dodd-Frank, companies must address whether they considered the most recent say-on-pay vote in making compensation decisions.

Because the CD&A explains the rationale behind pay decisions, it’s also a window into what the committee prioritized — and what they didn’t. Executives reviewing proxy statements from prospective employers can learn a great deal about how the compensation committee operates.

How Can Executives Engage Effectively With Compensation Governance?

Understanding committee dynamics isn’t just academic — it directly affects your ability to negotiate and protect your compensation.

What Should You Know Before Negotiating?

Before entering compensation negotiations with a public company, understand the company’s recent compensation history. Review past proxy statements to assess how the compensation committee has treated executives in similar roles, what performance metrics are typically used, and how the company has fared on say-on-pay votes. This background helps you evaluate whether your proposed package is realistic and defensible.

Equity compensation packages, including stock options and restricted shares, are especially important to examine carefully, as their value depends heavily on how vesting schedules and performance conditions are structured.

How Do Change-in-Control Provisions Get Negotiated?

Change-in-control provisions are typically negotiated at the employment agreement stage rather than after the fact. Compensation committees — and their advisors — have strong views about what’s acceptable in this area. Golden parachute arrangements that are too rich may face proxy advisor criticism and Say-on-Pay complications.

Getting these provisions right from the start requires understanding both what the committee is likely to approve and what legal protections you need. An employment attorney with executive compensation experience can help you navigate this balance.

How Do Clawback Policies Affect What You Negotiate?

Clawback provisions have become a standard feature of executive pay programs following SEC rules requiring listed companies to adopt policies for recovering erroneously awarded incentive compensation. Compensation committees are required to implement these policies, but the terms — including which events trigger recoupment and over what time period — may have room for negotiation.

Understanding the clawback framework embedded in your employment agreement or equity award documents is essential before you sign anything.

When Should You Involve Legal Counsel?

Executive employment agreement negotiations are not the place to go it alone. Compensation committees and their advisors are well-represented, and what looks like a standard offer may contain provisions that significantly limit your rights or protections.

Legal counsel experienced in executive compensation can help you understand the governance framework you’re operating within, identify negotiating leverage, and ensure that your executive severance and retirement protections are properly documented and enforceable.

How Is Corporate Governance Shaping the Future of Compensation Committees?

The relationship between corporate governance standards and executive compensation continues to evolve. Institutional investors are pushing for better alignment between pay and long-term performance, clearer disclosure, and more meaningful committee accountability.

Recent SEC roundtable discussions have focused on whether current disclosure requirements are producing information that investors actually find useful, or whether the volume and complexity of disclosures is obscuring more than it reveals. At the same time, proxy advisory firms are extending their pay-for-performance evaluation windows from three to five years — a shift that rewards companies whose compensation programs emphasize long-term value creation over short-term metrics.

For executives, these trends underscore why it’s valuable to understand how the broader executive compensation landscape is shifting — and how those shifts affect the parameters within which your compensation will be evaluated.

What Are the New York-Specific Considerations?

New York is home to many of the nation’s largest public companies, and executives negotiating compensation packages with NYSE-listed firms are operating in a particularly scrutinized governance environment. The SEC’s enhanced independence rules for compensation committees — which were adopted in response to Dodd-Frank and apply to NYSE-listed companies — set a higher bar for committee independence than exists for smaller or private employers.

New York also has strong employment law protections that can affect how certain compensation components are structured. For example, agreements about deferred compensation, bonus payments, and non-compete clauses all interact with New York’s employment law framework in ways that an experienced employment attorney can help you navigate.

Ready to Navigate Your Executive Compensation Negotiation?

Understanding board compensation committee dynamics is only part of the equation. Turning that knowledge into a better compensation outcome requires a legal strategy tailored to your specific situation. If you’re entering an executive role, evaluating a new offer, or dealing with a compensation dispute, Nisar Law Group can help. Our employment law attorneys have extensive experience advising executives on compensation matters across New York and New Jersey. Contact us today for a consultation.

Frequently Asked Questions About Board Compensation Committee Dynamics

A board compensation committee is a subcommittee of a company’s board of directors responsible for overseeing executive pay programs. At public companies, the committee approves compensation for the CEO and senior executives, sets performance goals, evaluates executive performance, and produces the Compensation Discussion & Analysis included in the annual proxy statement. The committee also oversees equity compensation plans and ensures the company’s pay practices comply with SEC disclosure requirements.

Under NYSE and Nasdaq listing standards, compensation committee members must be independent directors — meaning they have no material financial relationship with the company beyond their board service. The independence standard for compensation committee members is stricter than the general director independence test, requiring the board to consider the director’s compensation sources and company affiliations in evaluating whether they can make independent judgments about executive pay.

Compensation committees often retain independent compensation consultants to benchmark executive pay against peer companies, advise on pay structure, and provide market data. Before engaging any consultant, the committee must assess their independence using six factors specified by SEC rules, including the fees paid to the consultant’s firm and any other services the firm provides to the company. While committees are not required to use independent consultants, they must evaluate independence before receiving advice.

A say-on-pay vote is a non-binding shareholder advisory vote on a company’s executive compensation program, required by the Dodd-Frank Act for most public companies at least every three years. While the vote doesn’t require companies to change their pay practices, a low approval rate signals shareholder dissatisfaction and typically prompts committee engagement with major investors. Proxy advisory firms like ISS and Glass Lewis issue recommendations on say-on-pay votes that significantly influence institutional investor voting.

Executives have the most leverage during the initial employment negotiation, before compensation parameters are set. Understanding how the company’s compensation committee has historically approached pay decisions — through proxy statement review — helps identify what’s realistic and where there may be flexibility. Legal counsel experienced in executive compensation can help identify negotiating leverage on items like change-in-control provisions, clawback terms, severance protections, and equity award conditions.

When a company receives low say-on-pay support, it’s generally expected to engage with shareholders to understand their concerns and demonstrate responsive changes in subsequent compensation cycles. Proxy advisory firms track whether companies respond adequately to negative votes; those that don’t may face recommendations to vote against compensation committee members in director elections. ISS recently clarified that it will consider a company’s good-faith engagement efforts even when direct shareholder feedback was difficult to obtain.

Private companies and smaller reporting companies are generally not subject to the same compensation committee requirements as large public companies. NYSE and Nasdaq listing standards apply only to listed companies. Private companies may have compensation committees or similar governance structures, but they’re not required to comply with SEC disclosure rules or stock exchange independence standards. That said, many private equity-backed companies and those preparing for an IPO voluntarily adopt governance practices modeled on public company standards.